Small Business Funding: Complete Guide to Raising Capital Successfully 🎯

Small business funding represents the lifeblood enabling entrepreneurs to launch, operate, and scale their ventures. Business funding for small business encompasses diverse capital sources—from personal savings through institutional investors—each serving specific growth stages and financial needs. Understanding this landscape empowers entrepreneurs to strategically access capital matching their circumstances.

The funding ecosystem has transformed dramatically. In 2026, technology and government programs democratize access to capital previously available only to connected entrepreneurs. This accessibility combined with traditional financing options creates unprecedented opportunity for serious business builders.

Small Business Funding Guide – 2026 Overview 📊

Government programs expanded dramatically: MSME schemes, startup grants, MUDRA loans (India-specific), SBA programs (USA)

Fintech disrupting traditional lending: Approval timelines compressed from weeks to hours

Alternative financing maturing: Revenue-based, invoice factoring, merchant cash advances gaining legitimacy

Angel networks democratized: Digital platforms connecting entrepreneurs globally

Crowdfunding validating concepts: Simultaneously funding and testing business ideas before scaling

Understanding Capital Requirements: Self-Funded vs. External Financing

Business funding for small business begins with ruthlessly honest assessment of capital needs. Different business stages demand different funding amounts, timelines, and source compatibility.

Pre-Seed Stage: Building Foundation Capital

Bootstrapping Your Venture: 🔨

Bootstrapping means growing your business using personal savings and reinvested revenue—eliminating external pressure while maintaining complete ownership. This approach develops disciplined financial habits, validates product-market fit authentically, and avoids premature scaling.

Bootstrapping reality:

Minimal capital required: $0-50K typical range covers MVP and initial operations

Zero dilution: Retain 100% business ownership permanently

Growth pace controlled: Founder dictates expansion rhythm without investor pressure

Survival instinct: Lean operations become organizational DNA

Trade-off: Bootstrapped businesses grow 40-60% slower than funded competitors—sometimes problematic in fast-moving markets.

Friends & Family Rounds: 👥

Raising $10K-100K from personal networks combines trust-based access with manageable capital for MVP development. This represents logical stepping stone after bootstrapping initial traction.

Success practices for relationship funding:

Formalize agreements legally: Written contracts prevent future relationship deterioration

Communicate risks transparently: Explain that 90%+ of startups fail honestly

Document terms clearly: Specify equity percentage, vesting schedules, exit scenarios

Maintain quarterly communication: Regular investor updates build confidence

Seed Stage: Validating Product-Market Fit

Government-Backed Programs: Lowest Cost Capital

Government programs globally distribute billions supporting small business owners—typically with minimal repayment or equity surrender. These represent most accessible funding sources for validated concepts.

Major government programs include:

Startup India Seed Fund Scheme: Up to ₹10 lakh non-dilutive grants

Pradhan Mantri MUDRA Yojana (PMMY): Microloans up to ₹10 lakh at subsidized rates

MSME loans: Collateral-free lending up to ₹1 crore

Industry-specific grants: Agriculture, manufacturing, tech startup support

Government funding characteristics:

Ultra-low interest: 4-8% typical (vs. 12-25% alternative lenders)

Extended repayment: 7-10 year terms reduce monthly burden

Zero dilution: Retain 100% business ownership

Lengthy approvals: 1-6 months typical timeline

Institutional Funding Sources: Banks, Angel Investors, Venture Capital

Business funding for small business increasingly involves institutional sources when capital needs exceed $50K. Understanding institutional financing proves essential for entrepreneurs pursuing scaled growth.

Traditional Bank Loans: Stability & Credibility

Bank Term Loans: 💳

Banks provide $50K-$1M+ loans with 6-8% interest, fixed repayment schedules over 3-10 years. These remain foundational financing sources despite fintech disruption.

Bank loan advantages:

Institutional credibility: Bank backing signals customer/supplier confidence

Favorable interest rates: 6-8% significantly lower than alternative lenders (12-25%)

Extended repayment terms: 7-10 years reduce monthly payment burden

Predictable costs: Fixed rates eliminate surprise rate increases

Bank loan disadvantages:

Strict credit requirements: Typically require 700+ credit score, 2+ years operation

Collateral demands: Real estate, equipment, or personal guarantee required

Lengthy approval timeline: 2-6 weeks standard process

Documentation burden: Extensive financial statements, tax returns, business plans

Bank loan approval reality: Only 25-30% of small business loan applications get approved.

Angel Investors: Capital Plus Strategic Value

Individual investors providing $25K-500K capital with strategic guidance, mentorship, connections. Angels represent crucial bridge capital between friends & family and institutional venture capital.

Angel investor characteristics:

Investment size: $50K-250K typical check amounts

Equity stake: 10-20% dilution common

Funding speed: 2-3 months from serious pitching

Added value: Mentorship, industry connections, credibility amplification

Finding angel investors in 2026:

AngelList: Global network of 750,000+ angels

Indian platforms: LetsVenture, IAN (Indian Angel Network)

Local angel groups: Regional investment syndicates

Pitch competitions: Business plan competitions attracting angel attendees

SBA Loans: Government-Backed Business Funding

SBA 7(a) Loans: Up to $5M at 7.5% interest, 10-year repayment. These loans combine government backing with extended terms enabling meaningful capital access.

SBA loan advantages:

Large capital amounts: Up to $5 million available

Favorable interest rates: 7.5% significantly lower than market rates

Long repayment terms: 10 years reduces monthly payments

Government guarantee: SBA guarantees 75-85% of loan amount

SBA loan disadvantages:

Slow approval process: Weeks to months typical timeline

Extensive documentation: Business plans, financial statements, personal tax returns

Personal guarantee required: Personal assets backing business loan

Eligibility restrictions: Specific business types excluded

Alternative & Creative Funding: Beyond Traditional Lending

Business funding for small business increasingly leverages creative alternatives preserving equity while accessing needed capital. These options suit businesses with revenue, specific inventory needs, or strong customer bases.

Crowdfunding: Validation Plus Funding Simultaneously

Rewards-Based Crowdfunding (Kickstarter, Indiegogo): 📱

Entrepreneurs raise $10K-500K by pre-selling products to crowds—simultaneously validating demand while funding development. This dual benefit (capital + market validation) makes crowdfunding increasingly popular.

Crowdfunding advantages:

Dual benefits: Capital AND genuine market validation simultaneous

Community building: Pre-customers become brand evangelists

Zero dilution: Retain 100% business ownership

Marketing multiplier: Extensive media coverage for successful campaigns

Crowdfunding reality: 37-40% of campaigns reach funding targets; success requires compelling story and strong marketing.

Invoice Factoring: Immediate Working Capital

Invoice Factoring: 📋

Sell unpaid B2B invoices for immediate cash (typically 80-90% of invoice value, fees 2-5%). This suits service businesses and manufacturers with strong invoicing but slow payment cycles.

Invoice factoring characteristics:

Speed: Cash within 1-5 days—fastest business funding available

Cost: 2-5% fees per transaction

No dilution: Zero equity surrender

Working capital: Solves cash flow gaps perfectly

Revenue-Based Financing: Flexible Repayment Models

Alternative to equity and debt—repay through percentage of monthly revenue (typically 5-10% until cap reached).

Revenue-based financing characteristics:

Capital amounts: $50K-$1M typical range

Repayment structure: 5-10% monthly revenue until cap ($150K-$500K total)

Dilution impact: Zero percent equity—retain complete ownership

Speed: 1-2 weeks funding typical

Best suited for: SaaS, subscription services, e-commerce with consistent revenue

Revenue-based advantages:

No equity dilution: Maintain complete business ownership

Flexible repayment: Slow months mean lower payments automatically

Investor alignment: Lender succeeds only if business succeeds

Accessible qualification: Revenue-based qualification easier than credit-based

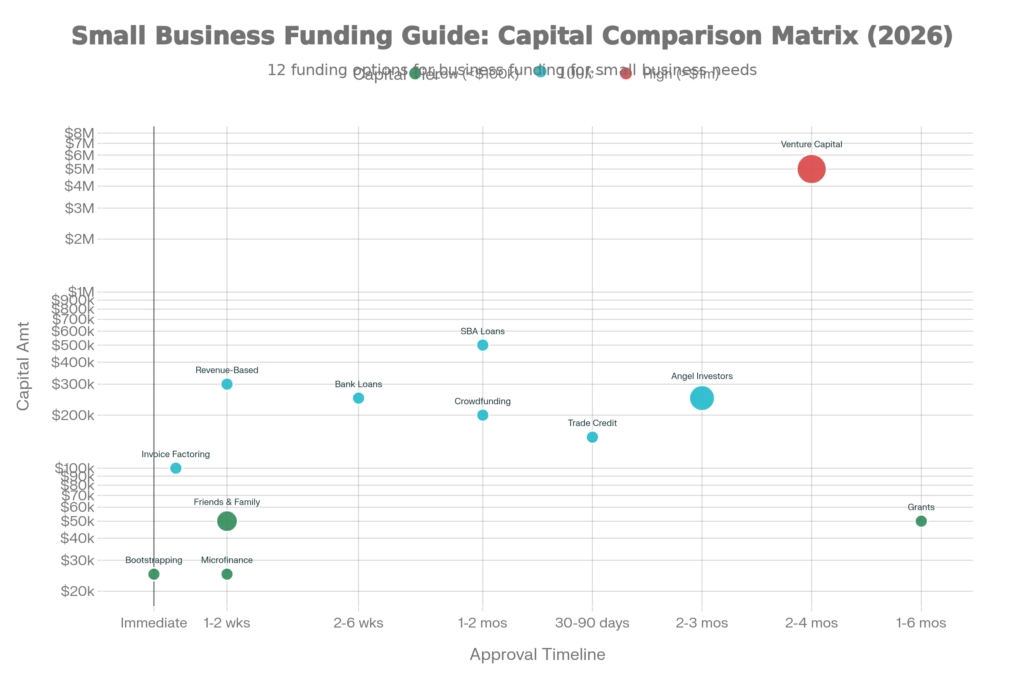

| Funding Type | Capital Range | Interest/Cost | Approval Speed | Dilution | Best For |

|---|---|---|---|---|---|

| Bootstrapping | $0-50K | 0% | Immediate | 0% | Initial MVP |

| Friends & Family | $10K-100K | 0-5% | 1-2 weeks | 5-15% | Seed validation |

| SBA Loans | $50K-5M | 7.5% | Weeks-Months | 0% | Working capital |

| Bank Loans | $50K-1M+ | 6-8% | 2-6 weeks | 0% | Expansion capital |

| Microloans | $5K-50K | 12-18% | 1-2 weeks | 0% | Quick startup cash |

| Grants | $5K-100K+ | 0% | 1-6 months | 0% | Innovation/growth |

| Angel Investors | $25K-500K | 0% | 2-3 months | 10-20% | Seed funding |

| Crowdfunding | $10K-500K | 0% | 1-2 months | 0% | Product validation |

| Invoice Factoring | Varies | 2-5% | 1-5 days | 0% | Cash flow gaps |

| Revenue-Based | $50K-1M | 5-10% revenue | 1-2 weeks | 0% | Revenue-stage growth |

Conclusion: Strategic Small Business Funding Enables Sustainable Growth 🚀

Small business funding guide success ultimately reduces to matching capital sources to specific growth stage, capital amount needed, and founder preferences regarding dilution and control. Bootstrapping suits lifestyle businesses prioritizing independence; venture capital accelerates growth but demands rapid scaling and profitability objectives.

Most successful entrepreneurs employ hybrid approaches—combining bootstrapping with government grants (zero dilution), then adding angel investors (moderate dilution) once product-market fit validates. This sequencing minimizes early dilution while providing capital for accelerated growth.

Strategic funding decision framework for 2026:

Do you value speed over equity retention? → Pursue angel investors or venture capital

Do you require $100K+ without dilution? → Combine SBA loans plus government grants

Do you want complete ownership indefinitely? → Bootstrap or use crowdfunding

Is consistent revenue already flowing? → Consider revenue-based financing

Do you have significant unpaid invoices? → Try invoice factoring for immediate cash

At StartupMandi, we recognize small business funding success requires expert guidance balancing growth ambitions with financial prudence. Explore our comprehensive capital raising playbook covering SBA loan optimization, government grant maximization, angel investor targeting. Discover our detailed business funding strategy guide analyzing all funding options with implementation roadmaps.

For entrepreneurs ready to capitalize growth strategically in 2026, small business funding access has never been more abundant or diverse. Visit our complete funding acquisition timeline walking through preparation through capital deployment. Connect with our funding advisors developing customized financing strategies aligned with your business model and growth trajectory.

The capital exists. The programs exist. Your move.

Disclaimer

This blog provides informational and educational insights about small business funding and capital raising options. It is not financial or investment advice. All funding decisions carry risk and financial obligation. Entrepreneurs should consult qualified financial advisors, accountants, and legal professionals before making binding funding decisions. Past fundraising success does not guarantee future results. Thorough due diligence on all funding sources is essential before commitment.

Frequently Asked Questions About Small Business Funding

Q1: Which small business funding option should I pursue first as a new business owner?

Start with bootstrapping and government grants ($0-100K combined). This preserves equity, validates business concept, and creates proof points attractive to angels and banks. Only pursue angel or bank capital after demonstrating meaningful traction and revenue.

Q2: How much equity should I expect to surrender in business funding for small business rounds?

Friends & family typically require 5-15% equity. Angel investors expect 10-20%. Government loans and grants dilute zero percent—maintain complete ownership. Revenue-based and crowdfunding also preserve 100% ownership.

Q3: What’s the realistic timeline from business concept to securing substantial capital ($100K+)?

Typical timeline spans 6-18 months. Three months validating concept, 3-6 months building traction, 2-3 months securing angel/bank funding. Fast-track companies achieve $100K+ funding in 6-12 months.

Q4: Can I secure small business funding without excellent personal credit?

Partially—government programs, crowdfunding, and alternative lenders focus on business metrics. However, SBA loans and bank lending require 700+ credit scores. Working to improve credit simultaneously strengthens overall funding prospects.

Q5: What single metric do lenders prioritize when evaluating business funding requests?

Monthly revenue growth trajectory matters most. Lenders want proof of 10%+ monthly growth demonstrating product-market fit and scalability. Beyond revenue, credit score, debt-to-income ratio, business plan quality, and collateral availability drive decisions.

Mariyam Bandookwala

i am a professional content writer with a strong focus on clarity, strategy, and audience engagement—helping brands communicate smarter and grow faster.