Infosys Buyback 2025: Share Price Impact & Investment Strategy — Complete Guide

Infosys has announced its fifth and largest-ever share buyback program worth ₹18,000 crore, opening for subscription on November 20, 2025, through November 26, 2025. The IT services giant will repurchase up to 10 crore fully paid-up equity shares at ₹1,800 per share, representing approximately 2.41% of total paid-up equity capital. At the current trading price of ₹1,542 (as of November 20, 2025), the buyback offer price represents a 16.7% premium, providing shareholders a meaningful opportunity to exit at elevated valuations. This comprehensive guide explores Infosys share price dynamics, buyback mechanics, participation strategies, and long-term implications for investors considering tendering their shares in this historic capital return initiative. [Source]

Understanding the Infosys Buyback: Scale and Strategic Rationale

The Record-Breaking ₹18,000 Crore Initiative represents Infosys ‘ commitment to returning surplus cash to shareholders while simultaneously managing its capital structure efficiently. The buyback dramatically exceeds Infosys ‘ previous four buyback programs: ₹13,000 crore (2017), ₹8,260 crore (2019), ₹9,200 crore (2021), and ₹9,300 crore (2022-23). This escalation reflects the company’s strengthened financial position, robust cash generation capability, and management’s confidence in execution despite challenging macroeconomic conditions. [Source]

Infosys undertook this massive buyback after carefully assessing medium-term strategic and operational cash needs while ensuring surplus funds are returned “in an effective and efficient manner in line with its capital allocation policy”. The timing proves significant: announced in September 2025 when Infosys share price had declined from its December 2024 all-time high of ₹2,006.45 to approximately ₹1,450-1,550, creating attractive valuation entry points for the company to retire shares. [Source]

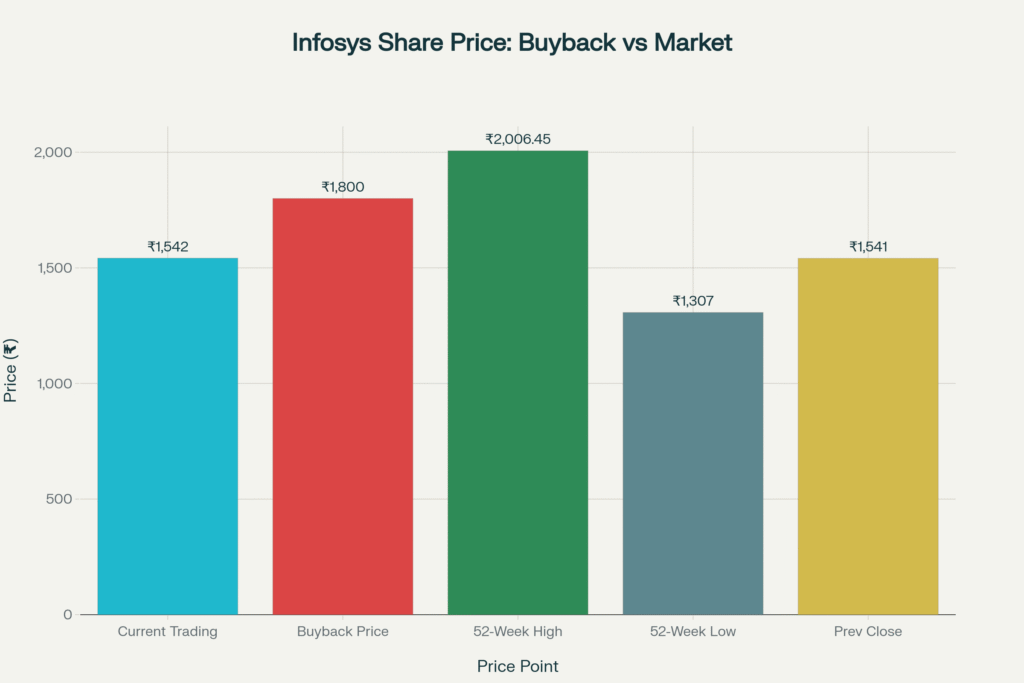

Infosys share price levels showing the ₹1,800 buyback price at a premium to current trading price, positioned between 52-week low and high

Infosys Share Price Dynamics: From Peak to Buyback Opportunity

To understand the buyback’s strategic context, examining Infosys ‘ recent share price performance proves essential. The stock achieved a 52-week high of ₹2,006.45 in December 2024, representing the highest level ever achieved by the company. However, from this peak, Infy share price experienced a 25% correction to ₹1,541 by November 2025, reflecting broader technology sector pressures, client budget reductions, and global economic uncertainties. [Source]

This correction, while significant, provides context for the buyback’s valuation logic. At ₹1,800, the buyback price sits between the 52-week low (₹1,307) and high (₹2,006.45), representing a fair entry point for the company to retire shares without appearing desperately cheap or expensively priced. The 16.7% premium to current trading prices incentivizes shareholders to participate, particularly retail investors seeking exit opportunities. [Source]

Infosys share price volatility reflects IT services sector challenges. Large clients including Daimler AG and Citigroup have reduced spending, impacting revenue growth. Daimler’s revenue with Infosys declined 8.5% in FY25—the first decline in three years after previously growing 40%+ annually. These headwinds contributed to the share price decline from December 2024 peaks to current levels.

Despite these challenges, Infosys Q2 FY26 results (announced October 16, 2025) demonstrated resilience. Consolidated revenue grew 8.6% year-on-year to ₹44,490 crore with net profit rising 13.2% to ₹7,364 crore. The company narrowed its FY26 revenue guidance to 2-3% in constant currency (from 1-3% previously), signaling management confidence. Operating margin remained stable at 21%, demonstrating pricing power and operational discipline despite revenue growth deceleration.

Buyback Mechanics: How It Works and Who Qualifies

Infosys ‘ buyback operates as a tender offer, meaning shareholders voluntarily submit shares for repurchase at the fixed price of ₹1,800. Understanding the mechanics proves essential for informed participation decisions:

Eligibility and Record Date

All shareholders holding Infosys equity shares on the record date of November 14, 2025 are eligible to participate. Critically, investors purchasing shares after November 13, 2025 cannot participate, as the record date had already passed. This creates an opportunity loss for new investors seeking buyback participation.

As of the record date, there were 25,85,684 eligible shareholders, indicating widespread retail and institutional participation. The company separated eligible shareholders into two categories with distinct benefits.

Small Shareholder Prioritization and Reservation

Recognizing retail shareholders’ interests, Infosys implemented a 15% reservation for small shareholders—those whose shareholding value does not exceed ₹2,00,000 on the record date. This reservation structure provides small shareholders preferential treatment, ensuring they receive allocation opportunities before general category shareholders.

Small shareholders benefit from favorable entitlement ratios: 2 shares for every 11 shares held (2:11 ratio) in the reserved category. Assuming full acceptance, small shareholders tendering 11 shares would receive ₹3,600 (2 shares × ₹1,800), a favorable allocation mechanism.

General Category and Acceptance Ratios

General category shareholders—those with holdings exceeding ₹2,00,000—face less favorable ratios of 17:706, meaning only 17 shares would be repurchased for every 706 shares tendered. This disparity reflects management’s intent to prioritize retail participation. [Source]

Acceptance ratios—the percentage of tendered shares the company repurchases—represent the critical unknown variable determining actual returns. If Infosys receives 100% participation, acceptance ratios could be as low as 15-20%, meaning only 15-20% of tendered shares would be repurchased. If participation reaches only 50%, acceptance ratios would approximate 30-40%.

The buyback’s attractiveness hinges directly on acceptance ratios. At 100% acceptance ratio, a ₹1,800 buyback price represents an 16.7% gain over current trading prices. At 50% acceptance, the gain remains 16.7% for accepted shares, but 50% of shares remain unaccepted, creating opportunity cost if Infosys share price subsequently declines. [Source]

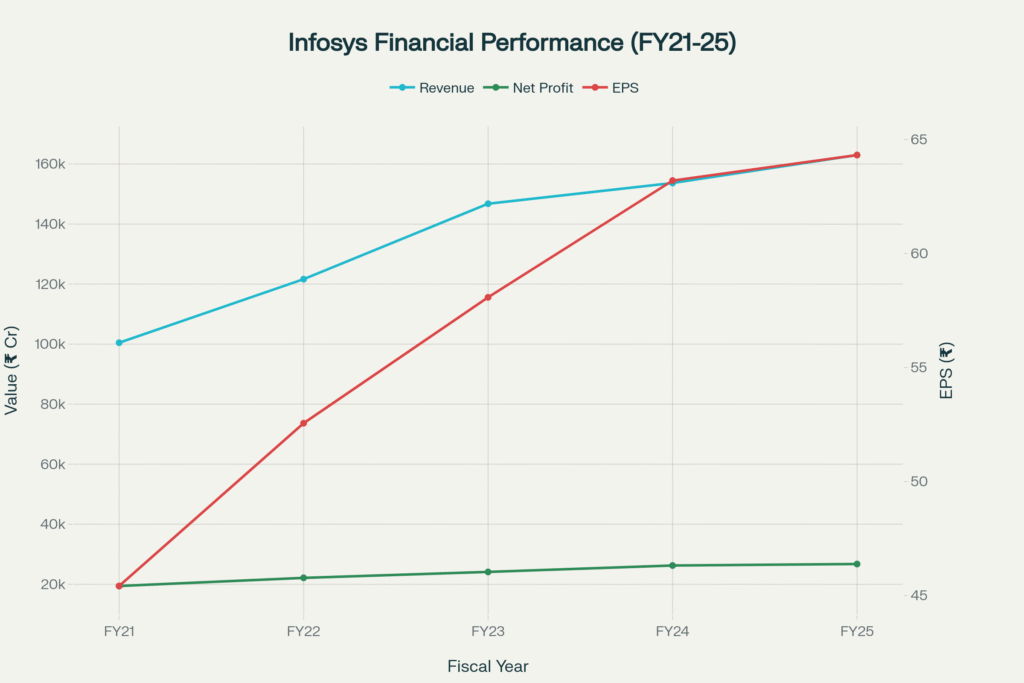

Infosys’ consistent financial growth from FY21 to FY25, with revenue reaching ₹162,990 crore, net profit at ₹26,750 crore, and EPS of ₹64.32

Financial Performance Underpinning the Buyback

Understanding why Infosys possesses adequate cash flow for this massive buyback requires examining financial performance. From FY21 to FY25, Infosys revenue grew from ₹100,472 crore to ₹162,990 crore—a 62.3% increase demonstrating strong underlying business growth despite recent headwinds.

Net profit expanded from ₹19,423 crore (FY21) to ₹26,750 crore (FY25), driven by operating leverage and favorable currency movements. Earnings per share increased from ₹45.42 to ₹64.32, a 41.7% expansion reflecting not only profit growth but also capital reduction through previous buybacks.

Free cash flow generation remains robust at approximately $1.1 billion quarterly (131% of net profit conversion ratio). This powerful cash generation validates management’s capital allocation policy: returning approximately 85% of cumulative free cash flow over five-year periods through dividends, buybacks, and special dividends.

Capital adequacy remains strong with debt-to-equity of just 0.08, indicating minimal leverage and substantial borrowing capacity if needed. The company carries ₹15,092 crore in reserves and surplus, providing financial flexibility for this buyback while maintaining strong capital buffers.

Investment Decision Framework: Should You Tender Shares?

Evaluating buyback participation requires weighing multiple factors:

Favorable Arguments for Participation

1. Premium to Market Price: At ₹1,800, the buyback offers a 16.7% immediate gain over November 20, 2025 trading prices. For risk-averse investors seeking near-term certainty, this immediate premium proves attractive versus holding shares at market prices.

2. Company Confidence Signal: Management’s decision to buyback during share price weakness indicates conviction in long-term value. Buyback announcements at depressed valuations—not at peaks—represent genuine capital allocation discipline.

3. Tax Efficiency (In Some Scenarios): For investors in zero tax brackets (those with insufficient income to be taxable), the buyback generates positive returns after tax, unlike dividend distributions subject to dividend distribution tax.

4. Reduced Equity Base: Share buybacks mechanically reduce equity share count, which mathematically increases earnings per share and return on equity metrics even if net profit remains unchanged. This EPS accretion benefits remaining shareholders.

Arguments Against Participation

1. Uncertainty on Acceptance Ratios: With only 2.41% of equity being repurchased against multiple eligible shareholders, acceptance ratios could be 15-20%. If your shares represent the 80-85% not accepted, you miss the buyback entirely while the stock continues trading.

2. Potential for Further Price Decline: The 52-week low stands at ₹1,307—if Infosys share price declines further below ₹1,800, non-accepted shares become financially impaired compared to the buyback offer.

Infosys share price levels showing the ₹1,800 buyback price at a premium to current trading price, positioned between 52-week low and high

3. Tax Implications: The buyback triggers capital gains tax on the profit between your purchase price and ₹1,800. If you purchased above ₹1,800, the buyback locks in losses. Additionally, TDS (Tax Deducted at Source) of 20% applies to buyback gains for non-zero tax category investors, though this can be adjusted in future tax filings.

4. Long-Term Growth Potential: If Infosys share price appreciates significantly above ₹1,800 in subsequent years, tendering at the buyback price represents opportunity cost. Historical precedent: Infosys shares traded at ₹2,006.45 just 11 months after the current buyback announcement.

Recent Market Context and Client Challenges

Client Consolidation and Budget Reductions present material risks to Infosys ‘ growth trajectory. Daimler AG reduced Infosys subsidiary revenue to $418 million (8.5% YoY decline) in FY25 despite historically strong 40%+ growth. Similarly, Citigroup reduced TCS E-Serve subsidiary revenue by 31%, indicating sector-wide client budget reductions.

Currency and Macro Headwinds further complicate the outlook. While Q2 FY26 demonstrated resilience with 13.2% net profit growth, this relied on favorable forex movements and cost optimizations partially offsetting revenue growth deceleration. Sustained rupee appreciation or further client budget cuts could pressure profitability.

However, AI-driven deal wins provide growth tailwinds. Infosys recorded $3.1 billion in large deal wins in Q2 FY26 (up 29% YoY), with 67% representing net new contracts. The company’s AI-first Topaz platform positions it strategically as clients seek digital transformation enabled by artificial intelligence.

Promoter Non-Participation Signals

Notably, Infosys promoters including Nandan M Nilekali and Sudha Murty (collectively holding 13.05% of equity) have chosen not to participate in the buyback. This decision—while not necessarily bearish—suggests promoters view current valuations as expensive rather than bargain opportunities, preferring to retain equity exposure.

Promoter non-participation contrasts with private investor expectations that buybacks at substantial premiums represent attractive accumulation opportunities. This divergence warrants consideration in decision-making.

Outbound Resources for Further Research

Investors seeking comprehensive information should consult:

- Infosys Investor Relations Portal: https://www.infosys.com/investors/ – Official financial statements, shareholder communications

- NSE/BSE Official Listings: https://www.nseindia.com/ and https://www.bseindia.com/ – Real-time trading data

- Financial Analysis Platforms: Moneycontrol, Yahoo Finance India – Real-time pricing and analyst ratings

- Tax Guidance: Consult with CA for TDS implications on your specific holding cost basis

Conclusion: Strategic Participation Framework

The Infosys ₹18,000 crore buyback presents a nuanced investment decision rather than a straightforward choice. The 16.7% premium to current trading prices appeals to risk-averse investors seeking certainty, while growth-focused investors might prefer retaining exposure for potential appreciation beyond the buyback price.

For small shareholders, the 15% reservation and favorable 2:11 entitlement ratios make participation relatively attractive. For large shareholders facing 17:706 odds, the uncertain acceptance ratio and potential opportunity cost may argue against participation.

Ultimately, the decision depends on your:

- Tax situation and cost basis

- Conviction on Infosys ‘ long-term growth prospects

- Risk tolerance regarding IT services sector headwinds

- Time horizon and cash needs

Whether the ₹1,800 buyback price proves attractive or regrettable will become clear in retrospect. At minimum, informed investors will carefully evaluate Infosys share price dynamics, financial fundamentals, and personal circumstances before tendering shares in this historic capital return initiative.