SBI Public Sector Bank Mergers

Strategic Consolidation & Lessons — A Detailed Story Analysis

The Indian public sector banking system has undergone a massive transformation over the past decade, with consolidation serving as the primary vehicle for reform and strengthening. At the forefront of this dramatic restructuring has been the State Bank of India (SBI) , which has orchestrated multiple waves of mergers that fundamentally reshaped India’s banking landscape.

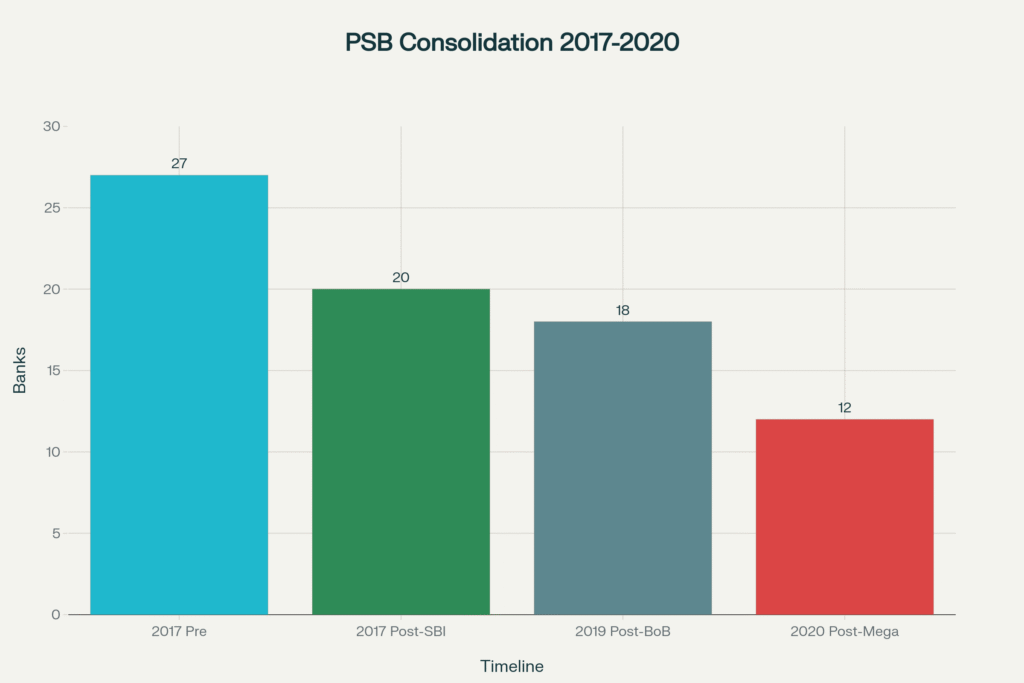

On April 1, 2017, SBI completed the largest merger in Indian banking history when it absorbed six entities—five associate banks and the Bharatiya Mahila Bank—creating a financial behemoth with ₹37 trillion in assets and over 250,000 employees. This milestone marked just the first chapter in a broader consolidation narrative that culminated in August 2019 when Finance Minister Nirmala Sitharaman announced an unprecedented nationwide banking reorganization plan, merging 10 additional public sector banks into four larger entities, reducing the total number of PSBs from 27 to 12 by April 2020.

Understanding these transformative mergers—their strategic rationale, implementation challenges, and long-term implications—reveals crucial lessons about financial institution consolidation, government policy effectiveness, and the future of public sector banking in India. [Source]

The Strategic Imperative: Why Indian Banking Needed Consolidation

The case for public sector bank consolidation in India rested on multiple compelling foundations. Fragmentation and Scale Disadvantage represented the primary driver, as India’s banking sector remained highly fragmented compared to peer economies. While China’s top five banks controlled approximately 36% of banking assets and the US maintained just three of the world’s ten largest banks, India’s banking landscape was scattered across 27 public sector banks competing with insufficient scale to compete globally. Many PSBs operated as sub-scale institutions, unable to achieve economies of scale, invest adequately in technology, or participate meaningfully in large corporate transactions and international banking. [Source]

The Non-Performing Asset Crisis constituted another critical motivation for consolidation. By March 2018, stressed assets across Indian PSBs had reached ₹10.35 lakh crore (roughly $12.3 billion at 2018 exchange rates), up from ₹3.23 lakh crore in March 2015. Gross NPAs exceeded 10% in several banks, creating systemic risks and consuming capital that could otherwise support productive lending. Government recapitalization efforts had already injected over ₹93,000 crore between 2009 and 2016, with additional allocations planned for 2017-19. Consolidation offered the prospect of pooling capital reserves and spreading NPAs across larger balance sheets with greater capacity to absorb losses. [Source]

Capital Efficiency and BASEL III Compliance added to consolidation urgency. BASEL III norms established stringent capital adequacy requirements that many smaller PSBs struggled to maintain. Merged entities could better optimize capital allocation, achieve higher capital adequacy ratios, and reduce the financial burden on government coffers by limiting required recapitalization. With India targeting the development of global-sized banks capable of supporting ₹300+ trillion in infrastructure investment needed for GDP growth, consolidation became essential policy. [Source]

The Government’s Fiscal Burden provided a macroeconomic dimension to consolidation. Ongoing requirements to recapitalize struggling PSBs diverted public resources from other priority investments in infrastructure, defense, and social programs. By creating larger, more efficient institutions through consolidation, the government hoped to reduce long-term recapitalization needs and improve returns on capital invested. [Source]

Indian public sector banking consolidation progression showing dramatic reduction from 27 banks in 2017 to 12 banks by 2020 through systematic mergers including SBI and mega-mergers

Phase One: The SBI Consolidation (2017-2017)

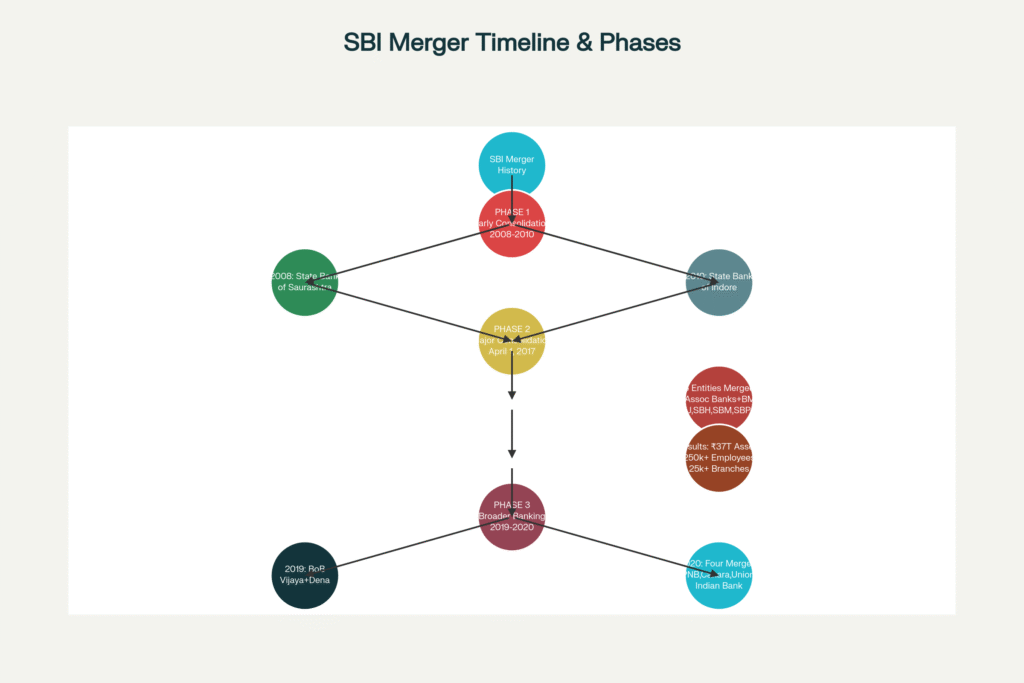

The SBI Merger Story begins with an earlier foundation-building exercise. Between 2008-2010, SBI had already merged two associate banks—State Bank of Saurashtra (2008) and State Bank of Indore (2010)—with itself, establishing the precedent for absorbing smaller entities. However, the April 1, 2017 mega-merger represented an exponential escalation in scale and ambition. [Source]

On February 13, 2017, the government announced that SBI would absorb five associate banks and the Bharatiya Mahila Bank, consolidating six separate organizations into a single entity. The five associate banks targeted were State Bank of Bikaner and Jaipur (SBBJ), State Bank of Hyderabad (SBH), State Bank of Mysore (SBM), State Bank of Patiala (SBP), and State Bank of Travancore (SBT). Each of these banks had evolved from regional subsidiaries of the State Bank of India, operating under historical autonomous structures despite SBI’s substantial ownership stakes. [Source]

The Mega-Merger Mechanics

The consolidation mechanism reflected careful structuring to minimize shareholder disruption. SBI offered share swaps with defined exchange ratios for each acquired bank. Shareholders of SBBJ received 28 SBI shares for every 10 shares held, while SBM shareholders received 22 SBI shares per 10 held. Similar carefully calibrated ratios applied to other associate banks based on their respective asset bases and valuations. This share-swap structure meant that shareholders received compensation through SBI shares rather than requiring cash outlays, preserving SBI ‘s liquidity.

The merger created a combined entity with ₹37 trillion in consolidated assets, propelling SBI into the top 50 global banks by asset size—a historic achievement for an Indian financial institution. The merged bank controlled over 25,000 branches and served approximately 500 million customers, making it one of the world’s largest banking networks by branch density. Employee strength expanded to approximately 250,000+, creating integration challenges related to organizational culture, compensation harmonization, and role consolidation. [Source]

The balance sheet pooling revealed substantial synergies. By combining reserve pools, SBI strengthened its capital adequacy ratios to 13.5%+, exceeding regulatory minimums and providing buffers for future lending expansion and NPAs. Asset quality improved as stronger SBI processes and credit standards were applied across the merged entity. The consolidated balance sheet’s size and diversification across geographies and customer segments reduced individual credit concentration risks. [Source]

Integration Challenges and Outcomes

Despite careful planning, the SBI merger implementation encountered significant integration challenges. Customer account migration and branch consolidation required sophisticated information technology coordination. Regional bank brands with century-old histories were dissolved into the national SBI umbrella, risking customer confusion and potential attrition in markets where regional brands held strong loyalty.

Employee integration proved particularly complex, with concerns about role redundancy, branch closures in overlapping markets, and harmonization of salary structures across different grade levels. Union representations and employee concerns about job security created pressures that management had to carefully navigate to maintain morale and productivity during the transition.

NPA Management remained an ongoing challenge even post-merger. While consolidation pooled problem assets and provided greater capital to absorb losses, it didn’t automatically resolve underlying credit quality issues. The merged entity faced continued pressure from inherited NPAs from associate banks, requiring persistent collection efforts and write-offs. [Source]

Despite these challenges, analysis of SBI ‘s post-merger performance reveals substantial improvements. Capital adequacy strengthened from pre-merger levels, providing stronger capital buffers against future shocks. Global competitiveness improved dramatically with SBI achieving a position among the world’s top 50 banks by assets, enabling participation in major international transactions previously inaccessible to smaller Indian banks. Operational efficiency began improving as duplicate functions were consolidated and technology platforms were harmonized.

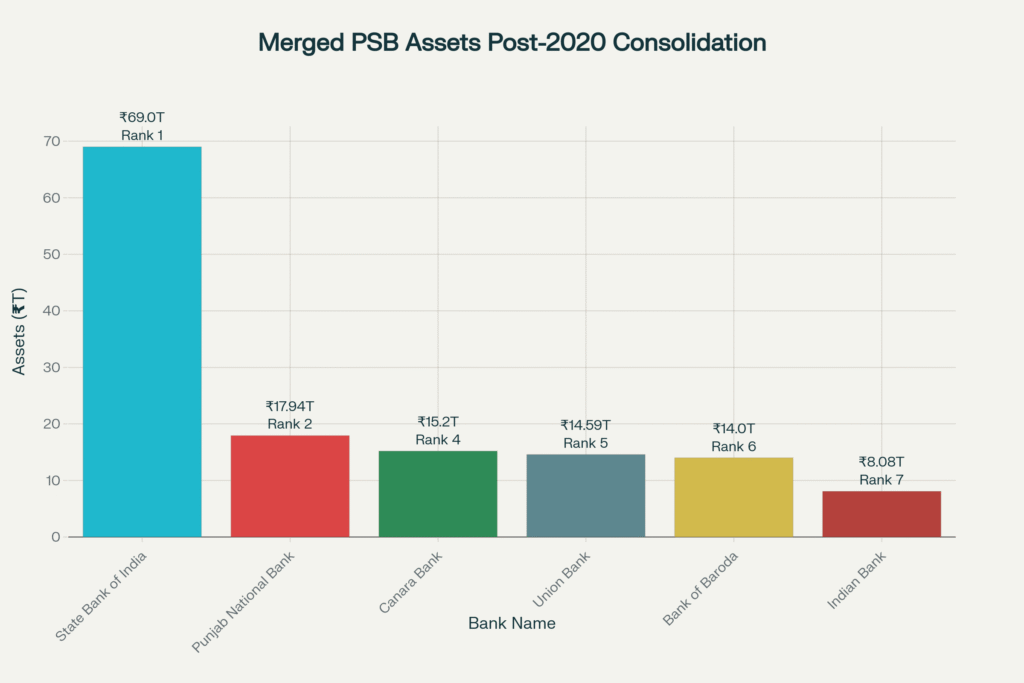

The six major merged public sector banks showing SBI’s dominance with ₹69 trillion in assets, followed by consolidated entities PNB, Canara Bank, Union Bank, and Bank of Baroda

Phase Two: The 2019 Announcement and Broader Banking Consolidation

On August 30, 2019—over two years after the successful SBI merger integration—Finance Minister Nirmala Sitharaman announced an even more ambitious consolidation plan affecting India’s entire public sector banking system. The announcement proposed merging 10 public sector banks into four larger entities, dramatically reducing banking fragmentation across the sector.

The Four-Way Consolidation Framework

The 2019 consolidation plan organized around four anchor banks, each absorbing one or more smaller institutions:

1. Punjab National Bank (PNB): Designated as the anchor for the second-largest PSB consolidation, PNB was assigned to absorb Oriental Bank of Commerce (OBC) and United Bank of India (UBI). Post-merger, PNB would become India’s second-largest public sector bank with combined assets of ₹17.94 lakh crore. The three-bank combination aimed to create a true global-sized competitor positioned immediately after SBI in India’s banking hierarchy.

2. Canara Bank: Designated to merge with Syndicate Bank, creating the fourth-largest PSB with ₹15.20 lakh crore in combined assets. Notably, Canara Bank had lower gross NPA ratios (8.77%), making it a relatively stable anchor for the integration despite Syndicate Bank’s historical challenges.

3. Union Bank of India: Tasked with absorbing both Andhra Bank and Corporation Bank, creating the fifth-largest PSB with ₹14.59 lakh crore in combined assets. Union Bank faced a higher challenge due to net NPA ratio of 6.85%—relatively elevated for a merger anchor—suggesting inherited asset quality issues would require active management.

4. Indian Bank: Designated to merge with Allahabad Bank, creating the seventh-largest PSB with combined assets of ₹8.08 lakh crore. Indian Bank’s lower NPA ratio of 3.75% positioned it favorably among merger anchors, despite absorbing Allahabad Bank’s legacy challenges.

Government Capital Infusion and Implementation

To support these mergers and strengthen merged entities’ capital adequacy, the government announced ₹55,250 crore in upfront capital infusion distributed across PSBs. PNB received ₹16,000 crore, Union Bank received ₹11,700 crore, Bank of Baroda received ₹7,000 crore (for its earlier 2019 Vijaya-Dena merger), Indian Bank received ₹2,500 crore, and Indian Overseas Bank received ₹3,800 crore. This massive capital injection—unprecedented in scale—aimed to preemptively strengthen balance sheets before merger integration’s stress periods.

The merged PNB , despite concerns about integration complexity, was projected to compete effectively with HDFC Bank (India’s largest private sector bank) and serve as India’s second-largest lender. The consolidation reduced the overall count of public sector banks from 27 (in 2017) to 12 by April 2020—a 55% reduction achieved in just three years.

Earlier Phase: Bank of Baroda Consolidation (2019)

Before the broader 2019 consolidation announcement, Bank of Baroda had already completed India’s first three-way bank merger in April 2019. BOB absorbed both Vijaya Bank and Dena Bank on April 1, 2019—marking a historic precedent for multiple simultaneous acquisitions.

This merger proved particularly complex due to the three-way integration requirements, backend system alignment, and customer account migration across disparate platforms. Vijaya Bank’s systems had to be migrated to BOB’s core banking solutions, followed by Dena Bank’s systems integration—a phased process requiring sophisticated project management. Despite these complexities, the BoB-Vijaya-Dena consolidation successfully created India’s fourth-largest bank and served as a validation exercise for the subsequent broader system-wide consolidations.

Impact Analysis: Financial Performance and Asset Quality Post-Mergers

The critical question regarding these massive consolidations centered on whether they achieved their stated objectives. Research examining post-merger performance across multiple metrics provides nuanced findings:

Asset Quality and NPA Management

Gross NPA reductions were observed across major merged entities post-2020, suggesting some improvement in asset quality management. PNB reduced its GNPA ratio from 15.84% pre-merger to 8.88% post-merger—a substantial 7-percentage-point improvement reflecting both improved credit processes and resolution of problem assets. Similarly, Union Bank achieved meaningful GNPA reductions, and Bank of Baroda demonstrated better handling of bad loans post-Vijaya-Dena merger.

However, research papers analyzing merged entity performance note significant variation in consistency, suggesting that while average NPA metrics improved, underlying issues persisted. Sharp variations in NPA ratios across post-merger periods indicated transitional inefficiencies, different risk profiles of absorbed banks requiring harmonization, and integration challenges affecting credit quality metrics. This pattern suggests that mergers provided temporary compression of NPAs through balance sheet expansion but didn’t definitively solve underlying credit risk management issues.

Capital Adequacy and Financial Stability

Merged entities demonstrated improved capital adequacy ratios, bolstered by government capital injections and balance sheet consolidation. SBI achieved capital adequacy of 13.5%+, well above BASEL III minimums, providing cushion for future credit expansion and shock absorption. Similar patterns emerged across merged PNB , Canara Bank , and Union Bank , where combined capital pools exceeded individual bank requirements.

This improvement in capital adequacy—driven by both consolidation and government recapitalization—strengthened banks’ capacity to expand lending to credit-starved sectors including infrastructure, small business, and retail segments.

Operational Efficiency and Cost Rationalization

Branch network optimization represented a significant post-merger initiative, with merged entities consolidating overlapping branch locations to eliminate redundancy. Union Bank and PNB underwent substantial branch rationalization, closing redundant branches while maintaining geographic coverage. This optimization reduced fixed costs and improved operational efficiency.

Technology platform consolidation created synergies through unified core banking solutions replacing multiple legacy systems. While implementation created temporary disruptions and required significant IT investment, unified platforms eventually delivered operational cost reductions and improved data integration.

However, research acknowledges that staff integration challenges and redundancy concerns created short-term operational friction, affecting employee morale and potentially slowing post-merger efficiency gains.

The six major merged public sector banks showing SBI’s dominance with ₹69 trillion in assets, followed by consolidated entities PNB, Canara Bank, Union Bank, and Bank of Baroda

The Case for Further Consolidation: SBI’s 2025 Position

As of November 2025, SBI Chairman Challa Sreenivasulu Setty has advocated for another phase of PSB consolidation, arguing that several remaining smaller PSBs remain sub-scale despite previous consolidation efforts. Setty’s explicit support for continued rationalization reflects recognition that while 2017-2020 consolidations created larger entities, six independent PSBs—UCO Bank, Punjab & Sind Bank, Indian Overseas Bank , Central Bank of India , Bank of Maharashtra , and Bank of India —remain insufficient in scale to compete effectively or serve India’s long-term credit requirements.

The economic justification for further consolidation remains compelling. India’s aspiration to reach developed economy status by 2047 requires bank credit expansion from current 56% of GDP to approximately 130% of GDP—supporting a projected 10-fold GDP increase to $30 trillion. Such credit expansion requires banking institutions of scale capable of mobilizing resources, extending large loans, and serving as trusted financial intermediaries for massive infrastructure and industrial projects. Current 12 PSBs, while larger than their predecessors, remain inadequate to the task when compared to Chinese and US banking systems that concentrate significantly greater share of banking assets within their largest institutions.

However, further consolidation faces practical constraints. Integration capacity of large banking organizations is limited—attempting simultaneous consolidation of multiple large banks risks integration failures, operational disruptions, and customer service failures. Regulatory and legal complexity increases exponentially with larger consolidations, requiring sophisticated coordination across regulators, creditors, and stakeholders. Political economy dimensions become increasingly challenging as consolidation affects larger constituencies of employees, smaller urban branches, and rural service commitments.

Lessons from the SBI and PSB Consolidation Experience

The comprehensive consolidation exercise spanning 2008-2020 and continuing advocacy for further consolidation in 2025 yields several critical lessons:

Lesson 1: Scale Matters, But Isn’t Everything

Consolidation successfully created larger institutions with enhanced capital adequacy and lending capacity. However, research demonstrates that size alone doesn’t guarantee profitability, efficiency, or asset quality. Smaller PSBs that merged into larger entities often carried legacy issues—high NPAs, weak credit processes, obsolete technology—that consolidation didn’t automatically cure. Addressing asset quality and operational inefficiency requires parallel institutional reforms beyond mere consolidation.

Lesson 2: Integration Complexity Increases Exponentially

SBI ‘s 2017 merger of six entities succeeded despite significant integration challenges. However, the three-way BOB -Vijaya-Dena consolidation and the subsequent multi-bank mergers highlighted how integration complexity grows non-linearly with each additional institution combined. Planning for second and third rounds of consolidation must account for exponentially greater integration challenges, potentially necessitating phased approaches rather than simultaneous mega-mergers.

Lesson 3: Government Capital Injections Must Accompany Consolidation

The ₹55,250 crore capital infusion announced in August 2019 proved essential to successful merger implementation. Without this preemptive recapitalization, merged entities would have faced capital adequacy pressures during the stress of merger integration. Future consolidations must budget for substantial government capital support—not as an indication of merger failure, but as recognition that integrating stressed balance sheets into stronger entities requires additional capital buffers.

Lesson 4: Technology Integration Cannot Be Overlooked

The successful migration of associate bank systems to SBI ‘s unified core banking platform, and comparable efforts across other merged entities, required sophisticated IT project management and substantial investment. Legacy systems cannot be quickly retired without creating operational risks. Technology integration must be sequenced carefully with multiple contingencies and extended timelines.

Lesson 5: Employee and Stakeholder Management Determines Success

The SBI merger’s relative success compared to some other consolidations reflected careful attention to employee concerns, union negotiations, and transparent communication about role changes and opportunities. Mergers that failed to adequately manage employee concerns faced strikes, protests, and sustained morale challenges that hindered integration. Future consolidations must allocate significant resources and time to stakeholder management, recognizing that human factors often determine implementation success or failure.

Lesson 6: Global Competitiveness Improvements Are Real But Gradual

SBI ‘s advancement to Forbes’ top 56 banks globally (from outside top 100) represents a genuine achievement enabled by consolidation. However, the lag between merger announcement and realized competitive improvements—several years of integration before operational benefits materialize—underscores that consolidation is a long-term strategic play, not a short-term performance fix.

Lesson 7: Complementary Reforms Are Essential

Consolidation must accompany parallel reforms in credit appraisal, risk management, corporate governance, and technology infrastructure. Mergers address scale deficiencies but cannot compensate for weak institutional fundamentals. The most successful merged entities combined consolidation with simultaneous improvements in credit processes, governance, technology, and personnel practices.

Challenges and Criticisms: The Consolidation Debate

Despite general support for consolidation, meaningful critiques deserve serious consideration:

Limited Private Sector Competition Impact: Critics argue that consolidating PSBs while private banks like HDFC Bank and ICICI Bank expand creates an asymmetric competitive landscape. If PSBs consolidate but remain less efficient than private competitors, customers may migrate to private alternatives, limiting consolidated banks’ ability to gain market share.

Equity and Rural Access Concerns: Smaller independent PSBs, despite inefficiencies, maintained branches in rural areas and served economically marginal segments that larger consolidated banks might deprioritize. Excessive consolidation risks reducing rural financial service availability.

Government Fiscal Burden: While consolidation theoretically reduces long-term recapitalization needs, massive upfront capital injections (₹55,250 crore in 2019 announcement alone) impose near-term fiscal pressure on government budgets already strained by infrastructure and defense spending.

Conclusion: Consolidation as Strategic Imperative

India’s public sector bank consolidation from 27 independent institutions in 2017 to 12 by 2020, spearheaded by SBI ‘s transformative 2017 merger and Finance Minister Sitharaman’s 2019 consolidation announcement, represents one of the most ambitious financial sector restructuring exercises globally. The strategic rationale remains compelling: creating banking institutions of scale necessary to finance India’s infrastructure ambitions, reducing systemic fragmentation, and improving competitiveness in global banking.

However, the consolidation experience also demonstrates that mergers are complex instruments with mixed outcomes. While consolidation successfully created larger institutions with enhanced capital adequacy and lending capacity, it hasn’t automatically resolved underlying asset quality issues, operational inefficiencies, or competitive weaknesses. Successful consolidation requires not just merger mechanics but sustained attention to integration, governance reform, technology modernization, and human capital management.

Looking forward, SBI Chairman’s 2025 advocacy for further consolidation suggests policymakers haven’t abandoned the consolidation agenda. Yet proceeding cautiously—with adequate time for previous integration efforts to mature, explicit acknowledgment of increasing complexity, and allocation of necessary resources—represents prudent policy. The consolidated PSB sector that emerges from this decade of transformation has potential to powerfully support India’s economic development, but only if consolidation is accompanied by genuine institutional reform, technological modernization, and sustained commitment to serving all customer segments, not just large corporates.