Mortgage Rates in US 2026: Where They’re Headed and What Buyers Should Know

Mortgage rates in US are still shaping what buyers can comfortably afford in 2026. The short answer is that rates are easing a little, but they remain high enough to keep monthly payments under pressure and affordability tight for many homebuyers. As a result, even small rate changes can have a noticeable impact on what buyers can qualify for and how much house they can afford.

The current mortgage market is moving lower in small steps rather than sharp drops. Therefore, buyers and refinancers may find better opportunities than earlier this year, but they still need to shop carefully, compare multiple offers, and keep an eye on the broader economic trend. In addition, the best approach is usually to focus on the full payment picture instead of the rate alone.

What Are Mortgage Rates in US?

Mortgage rates are the interest rates lenders charge on home loans, and they have a direct effect on your monthly payment, total interest cost, and overall buying power. In other words, even a small shift in rate can change how much home you can realistically afford.

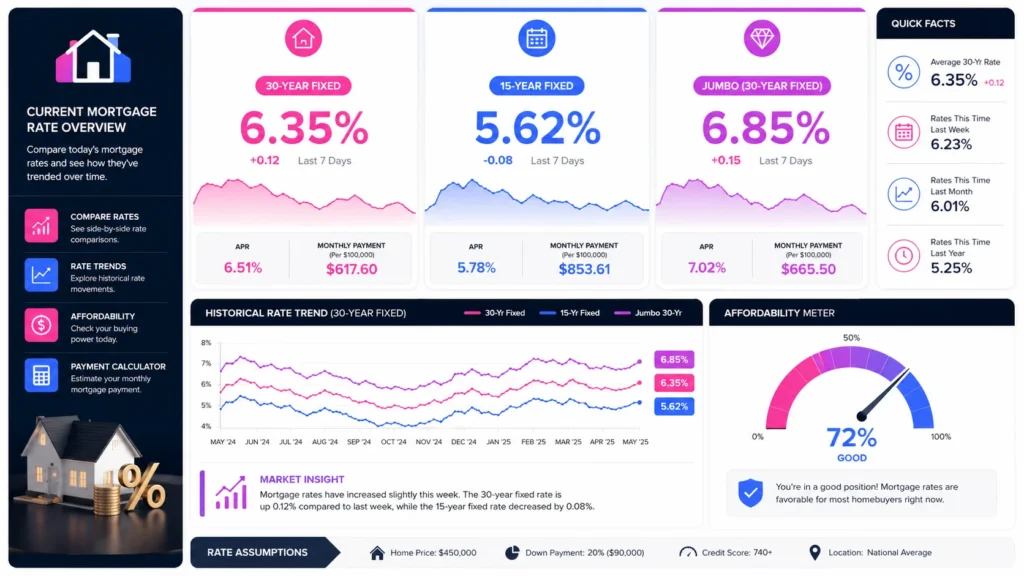

In the US, the most closely watched benchmark is the 30-year fixed mortgage rate. Recently, Freddie Mac reported that the average 30-year fixed rate eased to 6.43%, which marked a seven-week low. As a result, many buyers are watching this benchmark closely for signs of a better entry point.

Where Are Rates Now?

The US mortgage market has been drifting lower after months of volatility. FRED shows the 30-year fixed rate at 6.43% for the week ending July 2, 2026, while Trading Economics reports a similar reading of 6.58% for the week ending July 3, 2026.

That range matters because it shows the market is not locked at one exact number. It also shows how quickly weekly averages can shift depending on the data source and timing.

| Loan Type | Recent Rate | Source |

|---|---|---|

| 30-year fixed | 6.43% | Freddie Mac / FRED |

| 15-year fixed | 5.45% to 5.73% | Bankrate / Forbes |

| 30-year jumbo | 6.22% to 6.81% | Bankrate / Forbes |

Why Do Rates Matter?

Mortgage rates matter because even a small change can significantly affect your monthly payment. For buyers, that directly shapes affordability and also determines the size of the home you can realistically target. Moreover, a slightly lower rate may open the door to more options, while a higher one can quickly narrow the range.

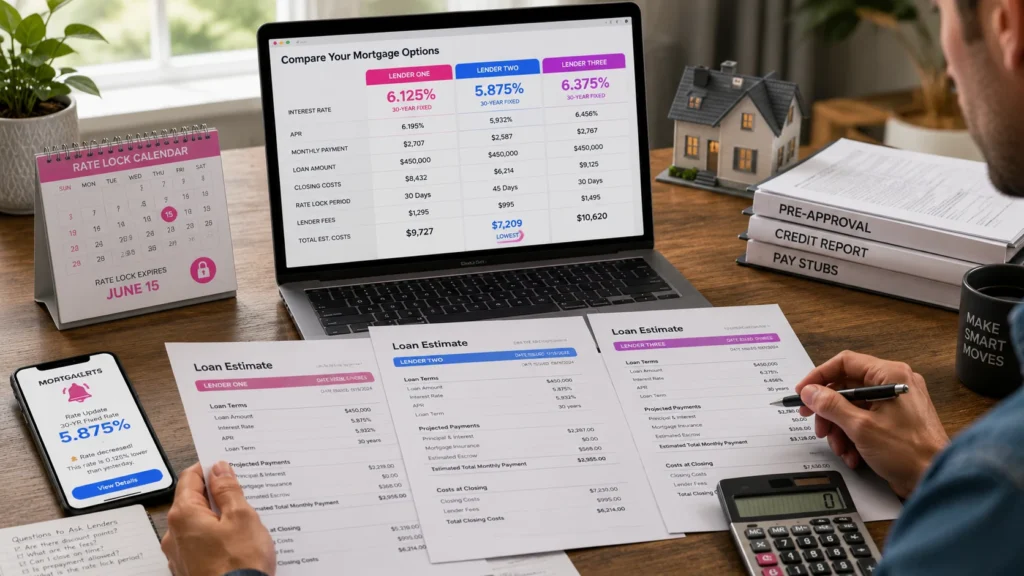

For refinancers, lower rates can create meaningful savings, but only if the closing costs and loan term actually make sense. That is why lenders often encourage shoppers to compare personalized quotes instead of depending on one advertised number. In addition, reviewing multiple offers gives you a clearer view of the true cost and helps you make a smarter decision.

What Is Driving Mortgage Rates in US?

Several forces are shaping mortgage rates in US right now :

- Inflation expectations.

- Federal Reserve policy.

- Treasury yields.

- Housing demand.

- Borrower competition across lenders.

Bankrate notes that rates are expected to drift slightly lower rather than plunge, while Fannie Mae’s forecast cited by Bankrate suggests rates may sit near 6% for much of 2026 and 2027. That suggests gradual improvement, not a sudden affordability reset.

“The consensus now is that mortgage rates will drift slightly lower.”

How Do Buyers Respond To Mortgage Rates?

Buyers are responding by shopping more carefully and adjusting expectations. Some are choosing smaller homes, longer timelines, or different loan structures to make the numbers work.

CNBC reported that mortgage rates hit their lowest level since 2022 in February 2026, yet homebuyer demand still remained soft because affordability was still a challenge. That is a reminder that lower rates help, but they do not fix the whole housing problem.

What Should Buyers Watch?

Buyers should watch three things closely :

- The 30-year fixed benchmark.

- The spread between fixed and adjustable loans.

- Monthly payment changes, not just headline rates.

If you are shopping now, it helps to compare the rate with the total payment. A slightly lower rate with higher fees may not always be the better deal.

How To Compare Mortgage Rates

Times Needed : 1 Day, 2 Hours, 0 Minutes

Estimated Cost : USD 0

Description : A practical process for comparing mortgage offers, estimating payment impact, and deciding when to lock a rate in 2026.

Steps :

- Check the benchmark rate

Review current 30-year fixed mortgage rates from trusted sources. This gives you a realistic starting point before you shop lenders. - Get personalized quotes

Ask multiple lenders for estimates based on your credit, down payment, and loan type. Personalized pricing is usually more useful than national averages. - Compare total costs

Look at rate, points, lender fees, and closing costs together. The cheapest headline rate is not always the cheapest loan. - Decide whether to lock

If rates look favorable and your closing timeline is close, a lock may reduce risk. If not, keep watching for short-term movement.

Tools Name

- Freddie Mac PMMS.

- FRED mortgage series.

- Bankrate mortgage calculator.

- LendingTree rate comparison.

Materials Name

- Credit score.

- Income documents.

- Loan estimate.

- Down payment details.

How Is Affordability Changing With Mortgage Rates?

Affordability remains tight because home prices and borrowing costs are still elevated at the same time. Even when rates improve a little, many buyers still feel the pressure of higher monthly payments and limited inventory. As a result, the market can still feel challenging even when headlines suggest improvement.

That is why the smartest mortgage strategy in 2026 is often to focus on payment comfort first. In other words, a home that fits your budget today is usually more valuable than waiting for the absolute bottom of the rate cycle. Moreover, choosing a payment you can comfortably manage can give you more stability and less stress over the long term.

Should Buyers Refinance When Mortgage Rates in US Change?

Refinancing can make sense when the new rate and loan terms improve your long-term financial picture. In fact, recent refinance trends are moving in the same general direction as purchase rates, which may create selective opportunities for some homeowners. As a result, it is worth checking whether a refinance could actually reduce your costs or improve your loan structure.

However, refinance math should always include closing costs, how long you plan to stay in the home, and whether you are shortening or extending the loan term. In addition, you should compare the monthly savings against the upfront expense before making a decision. If the numbers do not clearly work in your favor, waiting may be the smarter move.

Rate Snapshot Table

| Metric | Current Signal | Why It Matters |

|---|---|---|

| 30-year fixed | Around 6.43% to 6.58% | Main benchmark for buyers |

| 15-year fixed | Around 5.45% to 5.73% | Lower total interest, higher payment |

| Jumbo Loans | Around 6.22% to 6.81% | Helpful for high-priced homes |

| Market Outlook | Slight easing expected | Suggests gradual improvement |

Key Takeaways

- Mortgage rates in US are easing slightly, not collapsing.

- The 30-year fixed remains the most important benchmark.

- Affordability is still tight even when rates improve.

- Buyers should compare total loan costs, not just the headline rate.

- Refinancing may help, but only if the math works.

Next Steps

- Check this week’s benchmark mortgage rate.

- Request quotes from at least three lenders.

- Compare monthly payment, not only APR.

- Review whether to lock now or wait.

- Watch for affordability changes in the broader housing market.

FAQ

Recent benchmark readings show the 30-year fixed near 6.43% to 6.58%.

Analysts cited by Bankrate expect rates to drift slightly lower, with some forecasts near 6%.

It can be, if your monthly payment fits your budget and you find a home you can afford comfortably.

They often move in the same direction, but personalized refinance quotes can differ based on your profile.

They move with economic data, bond yields, inflation expectations, and lender pricing.

Compare monthly payment, fees, loan term, and long-term interest together.

Only if waiting still fits your housing timeline and personal budget.

Yes. Even a small move can affect your monthly payment and total interest over time.

Conclusion

Mortgage rates in US are showing signs of easing, but the market is still uneven and affordability remains a real challenge. For buyers, the smartest approach is to compare offers carefully, watch the full payment math, and move forward when the loan truly fits the budget. In addition, staying informed on broader market trends can help you make a better-timed decision.

For more useful updates and related topics, you can also explore StartupMandi Global for additional insights and market coverage.

Few Links Suggestions for more Research & Facts Check

- Mortgage Rates Ease to 6.43% — useful benchmark data.

- US 30-year Fixed Mortgage History — useful historical series.

- Bankrate Mortgage Rate Analysis — useful market outlook.

- Mortgage Rate Update from Forbes Advisor — useful rate snapshot.

- CNBC Coverage on Mortgage Demand and Affordability — useful affordability context.

Resources

- Freddie Mac Mortgage Rates — benchmark weekly mortgage data.

- FRED 30-Year Fixed Mortgage Series — historical US mortgage rate data.

- Bankrate Mortgage Rates — current lender marketplace context.

- NerdWallet Mortgage Rates — rate comparison and consumer guidance.

- LendingTree Mortgage Rates — personalized rate shopping.