Sale!

Original price was: ₹49,999.00.₹24,999.00Current price is: ₹24,999.00.

Sale!

Original price was: ₹9,999.00.₹3,999.00Current price is: ₹3,999.00.

Sale!

Original price was: ₹49,999.00.₹29,999.00Current price is: ₹29,999.00.

Sale!

Original price was: ₹49,999.00.₹29,999.00Current price is: ₹29,999.00.

Sale!

Original price was: ₹999.00.₹499.00Current price is: ₹499.00.

Sale!

Original price was: ₹99,999.00.₹49,999.00Current price is: ₹49,999.00.

Sale!

Original price was: ₹29,999.00.₹11,999.00Current price is: ₹11,999.00.

Sale!

Original price was: ₹29,999.00.₹19,999.00Current price is: ₹19,999.00.

Sale!

Original price was: ₹24,999.00.₹9,999.00Current price is: ₹9,999.00.

Sale!

- Select options This product has multiple variants. The options may be chosen on the product page

Price range: ₹11,999.00 through ₹59,999.00

Sale!

Original price was: ₹3,999.00.₹399.00Current price is: ₹399.00.

Sale!

Original price was: ₹5,999.00.₹3,999.00Current price is: ₹3,999.00.

Sale!

- Select options This product has multiple variants. The options may be chosen on the product page

Price range: ₹499.00 through ₹4,999.00

Sale!

- Select options This product has multiple variants. The options may be chosen on the product page

Price range: ₹44,999.00 through ₹294,999.00

Sale!

Original price was: ₹8,999.00.₹7,499.00Current price is: ₹7,499.00.

Sale!

Original price was: ₹3,999.00.₹1,999.00Current price is: ₹1,999.00.

New

Blockchain India Challenge – Get Up to ₹50 Lakh

Ministry of Electronics and Information Technology (MeitY), Government of India (implemented by Centre for Development of Advanced Computing – C-DAC)

- Idea Stage, Prototype Stage, MVP Stage

- March 27, 2026

New

Blockchain India Challenge – Get Up to ₹50 Lakh

Ministry of Electronics and Information Technology (MeitY), Government of India (implemented by Centre for Development of Advanced Computing – C-DAC)

- Idea Stage, Prototype Stage, MVP Stage

- March 27, 2026

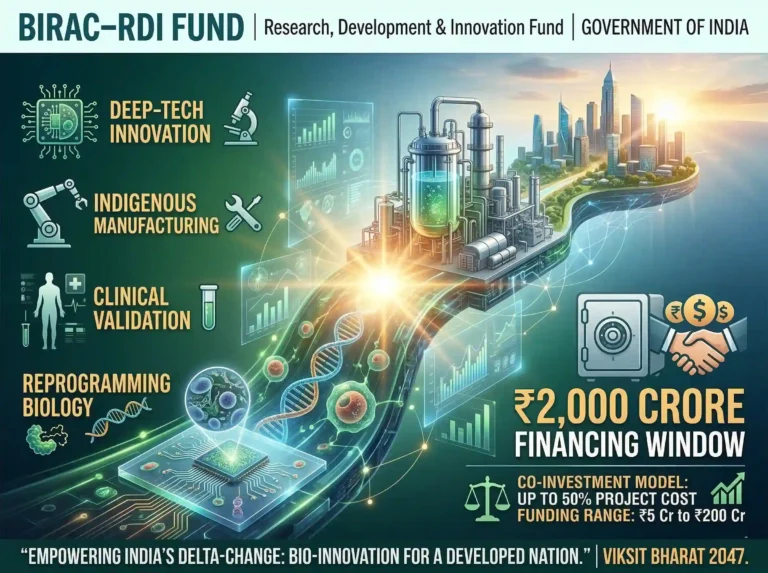

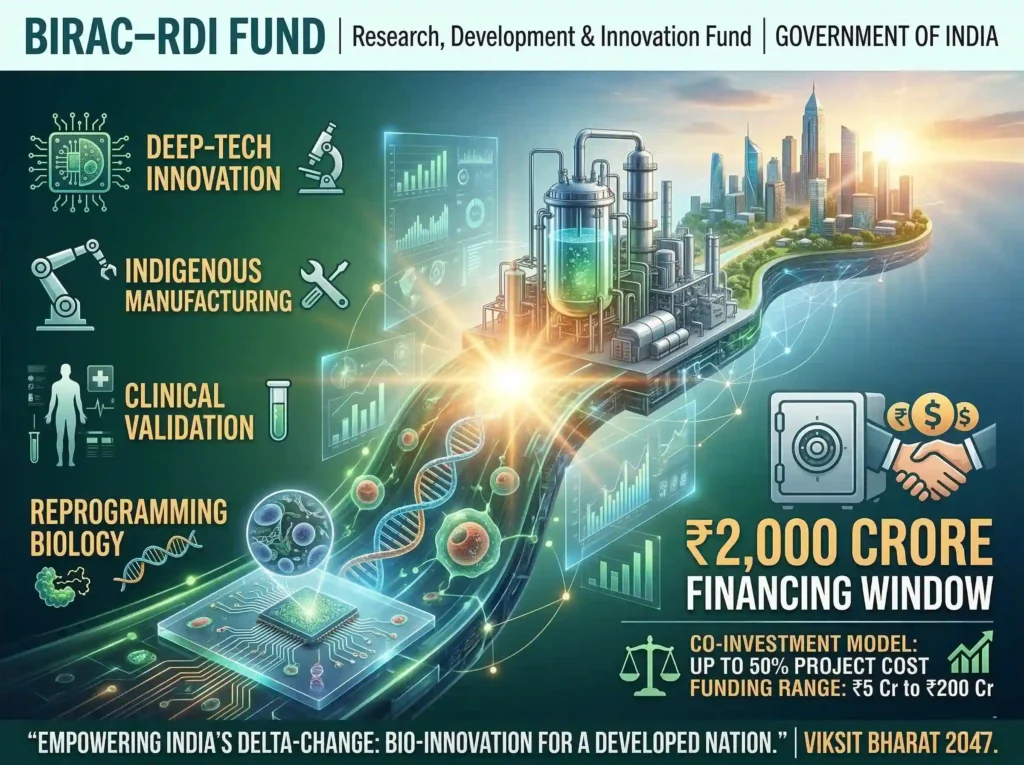

New

BIRAC–RDI Fund – Research, Development and Innovation Fund

Delta Change Challenge for Biotech Innovation – Biotechnology Industry Research Assistance Council (BIRAC), under Department of Biotechnology (DBT)

- MVP Stage, Early Revenue Stage, Growth Stage

- March 31, 2026