How to manage finances as a professional with strategic planning

How to manage finances as a professional is a skill that transforms your entire career trajectory. Many professionals earn excellent salaries yet struggle financially because they lack a clear financial strategy. When you take control of your money today, you avoid debt tomorrow and build lasting security. Additionally, smart financial choices early in your career create compound wealth over decades. Therefore, understanding budgeting, saving, and investing represents one of the most powerful investments in yourself.

Key takeaways you’ll discover:

Create a realistic budget using the proven 50/30/20 allocation method

Build an emergency fund that protects against unexpected financial shocks

Develop sustainable investment strategies for long-term wealth accumulation

Track spending and eliminate unnecessary expenses with actionable systems

Make informed financial decisions aligned with your personal goals and values

ASSESS YOUR FINANCIAL FOUNDATION

Evaluate Your Current Financial Position Before Moving Forward

Your financial journey begins with honest self-assessment. First, understand your complete income picture including salary, bonuses, and side income streams. Next, list all fixed expenses such as rent and insurance. Then, identify variable expenses like dining and entertainment. This thorough evaluation reveals exactly where your money flows each month. Furthermore, checking your credit score provides crucial insight into your financial health.

Know Your Take-Home Pay Accurately

Most professionals mistake their gross salary for their actual available funds. Instead, calculate your true take-home pay after taxes and deductions. This number forms the foundation of your realistic budget. Working with incorrect figures leads to overspending and financial disappointment. Fact: Many young professionals underestimate their deductions by 15-20%, causing serious budgeting errors. By knowing your exact monthly cash flow, you create a budget that genuinely works.

Track All Your Expenses Systematically

Monitoring spending habits reveals surprising patterns in your financial behavior. Use apps, spreadsheets, or bank statements to document every transaction. Categorize expenses into necessities, discretionary items, and savings contributions. This data-driven approach helps identify budget leaks and wasteful spending.

Key insight: Most professionals discover they can reduce expenses by 10-15% through conscious tracking alone.

CREATE A STRATEGIC BUDGET FRAMEWORK

Build a Budget That Supports Your Financial Goals Effectively

A well-designed budget is your personal financial roadmap and accountability system.

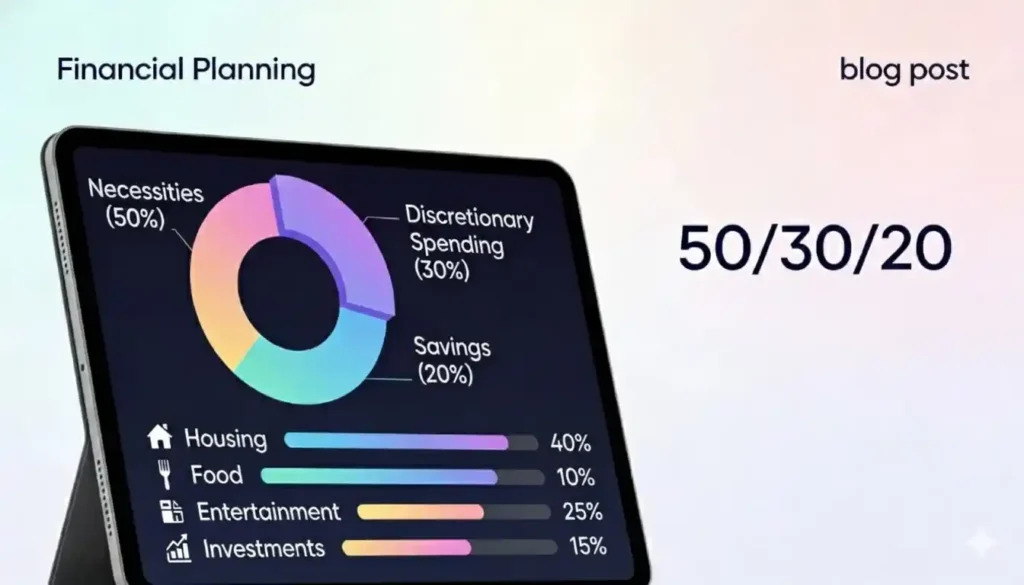

The 50/30/20 rule provides a simple, proven framework for most professionals.

- Allocate 50% of after-tax income toward necessities like housing, utilities, and groceries.

- Dedicate 30% to discretionary spending such as entertainment and dining out.

- Reserve 20% for debt repayment and savings contributions.

This balanced approach ensures you cover essentials while enjoying life and building wealth.

Implement the 50/30/20 Budget Model

50% for necessities: This covers rent or mortgage, utilities, groceries, transportation, and insurance. These are non-negotiable expenses that keep your life functioning smoothly.

30% for discretionary spending: Allocate this portion to entertainment, dining out, hobbies, and personal purchases. This maintains your quality of life and prevents financial burnout.

20% for savings and debt repayment: This crucial portion funds your emergency account and investment goals. If you carry debt, prioritize paying it down aggressively. Once debt-free, redirect this entire 20% toward long-term wealth building.

Adjust Your Budget to Match Your Lifestyle

The 50/30/20 framework works well for most professionals, yet your personal situation may differ. If you live in an expensive city, your housing costs might exceed 50%, requiring adjusted percentages. Similarly, if you have dependents or student loans, your discretionary allocation might shrink. The key is creating a budget you’ll actually follow consistently. Remember: A flexible budget you maintain beats a perfect budget you abandon.

| Budget Category | Percentage | Examples |

|---|---|---|

| Necessities | 50% | Rent, utilities, groceries, insurance |

| Discretionary | 30% | Entertainment, dining, hobbies |

| Savings & Debt | 20% | Emergency fund, investments, loan payments |

BUILD WEALTH THROUGH SAVINGS AND SMART INVESTING

Create Financial Security Through Emergency Funds and Strategic Investments

A truly secure financial foundation includes both defensive and offensive strategies. First, build an emergency fund that covers three to six months of living expenses. This safety net prevents debt spiral when unexpected expenses arise.

Meanwhile, start investing consistently to build long-term wealth through compound growth. When you combine emergency savings with regular investments, you create resilience and opportunity simultaneously.

Establish Your Emergency Fund as Priority One

An emergency fund prevents financial disasters from becoming catastrophic. Medical emergencies, job loss, or car repairs can destroy finances lacking this protection.

Aim to save ₹50,000 to ₹200,000 depending on your monthly expenses initially. Start small—even ₹5,000 monthly contributions build quickly over time.

Once established, treat your emergency fund as untouchable except for genuine emergencies.

Begin Investing Early to Maximize Compound Growth

The power of compound interest rewards early investors tremendously. Investing just ₹10,000 monthly from age 25 versus age 35 creates dramatically different retirement outcomes. Consider mutual funds, stocks, and retirement accounts available in India like PPF and NPS. Diversifying across asset classes reduces risk while improving long-term returns. Truth: Starting investments early matters far more than the amount invested initially.

Eliminate Debt Strategically

If you carry existing debt, develop a repayment strategy immediately. The snowball method pays smallest debts first for psychological momentum. The avalanche method targets highest-interest debt first for mathematical efficiency. Choose whichever approach keeps you motivated and consistent. Once debt-free, redirect those payments toward investment accounts.

Conclusion

How to manage finances as a professional ultimately means taking responsibility for your financial future today. By assessing your current position, creating a realistic budget, and investing consistently, you transform your financial life. These strategies don’t require earning more money—they require spending more wisely. Start implementing one strategy this week, then add another next month. Over time, these small changes compound into significant wealth and security. The best time to start managing your finances was yesterday; the second-best time is today.

Disclaimer: StartupMandi is not a SEBI-registered research Analyst or Investment Advisor. This content is for educational and informational purposes only and should not be construed as financial or investment advice. Please consult a qualified financial advisor before making any investment decisions.

FAQs

Q1: How much should I keep in my emergency fund?

A: Experts recommend saving three to six months of living expenses in an easily accessible account. Calculate your monthly expenses including rent, utilities, food, and insurance, then multiply by three to six. Start smaller if this feels overwhelming, gradually building toward the full amount. Your specific emergency fund target depends on job stability, family obligations, and personal comfort level.

Q2: Is budgeting necessary if I already earn a good salary?

A: Yes, absolutely. Income level doesn’t prevent overspending without conscious budgeting. Many high earners live paycheck-to-paycheck because they lack spending discipline. Budgeting ensures your income aligns with your values and goals rather than defaulting to unconscious spending. The 50/30/20 rule works equally well for ₹50,000 and ₹500,000 monthly incomes.

Q3: What’s the best investment option for beginners?

A: Begin with low-risk options like mutual funds, which provide professional management and diversification. Index funds track market performance with minimal fees, making them ideal for passive investors. Consider Systematic Investment Plans (SIPs) to invest fixed amounts monthly, removing emotion from investing. Once comfortable, gradually explore stocks, bonds, and real estate based on your risk tolerance.

Q4: Should I invest before paying off all my debt?

A: This depends on interest rates and the type of debt. High-interest credit card debt above 18% should be prioritized for repayment. Lower-interest loans like home mortgages or education loans might warrant splitting efforts between repayment and investing. Generally, balance aggressive debt payoff with modest investing to start building wealth immediately.

Q5: How often should I review and adjust my budget?

A: Review your budget monthly to track spending and quarterly to make adjustments. Major life changes—new job, marriage, children—require immediate budget revision. Seasonal variations in expenses should also influence quarterly reviews. Most professionals benefit from annual comprehensive budget overhauls comparing actual spending to planned allocations.

Referring Blog & Fact Sources

Here are authoritative resources for deeper financial guidance and professional insights:

-

Native Teams: How to Manage Money for Young Professionals – Comprehensive money management strategies and budgeting techniques

-

WorkAssist: How to Manage Finance as a Working Professional in India – India-specific financial planning and professional money management

-

AAFMAA Trust: 7 Steps to Financial Fitness – Structured financial planning methodology and wealth building framework

-

Reserve Bank of India Financial Literacy Resources – Official guidelines on investment and financial planning in India

-

National Institute of Securities Markets Educational Resources – Professional development and financial education for Indian professionals

Arshia Jahan

Digital Marketing and SEO professional, focused on content strategy & optimizing content, improving search rankings, and delivering results through smart, audience-focused strategies. As a Content Strategist and SEO professional, I believe that search engines don't buy products—people do. By blending technical SEO precision with a human-first content approach. I provide readers with the strategic blueprints needed to scale in a competitive digital world.