PSU Banks Merger: Government Plans Second Major Consolidation Round

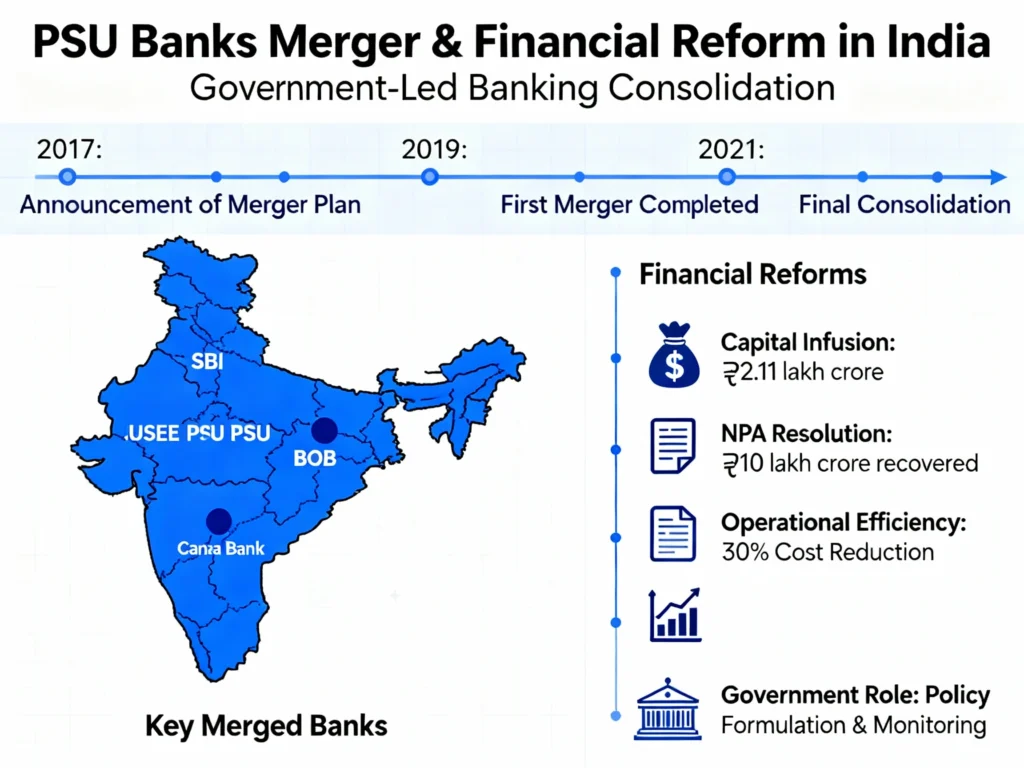

The Indian government is seriously considering another round of psu banks merger, which could reshape the country’s banking landscape once again. After reducing public sector banks from 27 to 12 between 2017 and 2020, authorities now plan to consolidate further—potentially bringing the number down to just six mega entities. This proposed psu banks merger has sparked intense debate about whether bigger banks truly mean better banking, especially when employee morale and cultural integration become critical success factors.

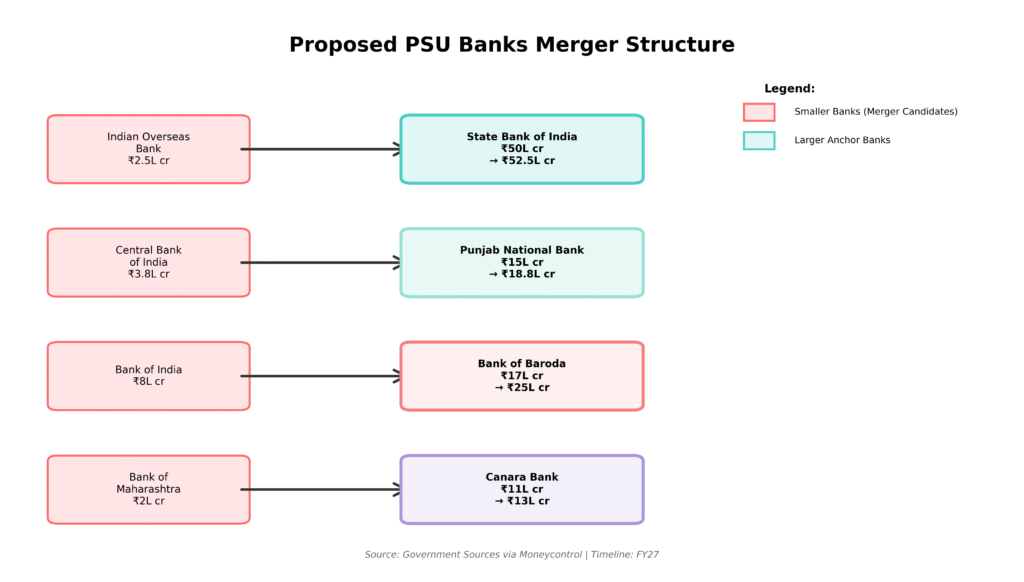

According to recent reports, the psu banks merger plan targets smaller lenders like Indian Overseas Bank, Central Bank of India, Bank of India, and Bank of Maharashtra for absorption into larger banks such as SBI, Punjab National Bank, and Bank of Baroda. While policymakers argue that scale matters for global competitiveness, banking veterans warn that previous psu banks merger attempts reveal a more complex reality—one where human factors often determine success or failure more than balance sheet arithmetic.

PSU Banks Merger: Government Plans Second Major Consolidation Round

Why Another PSU Banks Merger Makes Sense (On Paper)

The logic driving this psu banks merger proposal appears straightforward enough. Larger banks enjoy economies of scale, stronger capital buffers, and wider geographic reach. They can fund massive infrastructure projects, invest heavily in digital transformation, and compete more effectively with private sector giants like HDFC Bank and ICICI Bank. For regulators and policymakers, supervising six well-capitalized institutions proves far easier than monitoring twelve unevenly governed entities.

Globally, banking systems in economic powerhouses like China, Japan, and South Korea are dominated by a handful of mega banks that drive growth and innovation. India’s ambition to become a $5-trillion economy demands financial institutions capable of supporting that scale. The proposed psu banks merger aligns with NITI Aayog recommendations suggesting that only a handful of large PSBs—including SBI, PNB, BoB, and Canara Bank—should remain under full government control.

Beyond operational efficiency, this psu banks merger strategy responds to competitive pressure from fintechs and digital-first challengers. Private banks have steadily gained market share while public sector lenders struggle with legacy systems and bureaucratic processes. By consolidating, the government hopes to position PSBs strategically rather than spreading resources thin across multiple medium-sized entities.

PSU Banks Merger: Government Plans Second Major Consolidation Round

The Human Cost Nobody Talks About: Lessons from Past PSU Banks Merger

Here’s where theory meets uncomfortable reality. India’s first major psu banks merger happened way back in 1993, when Punjab National Bank absorbed New Bank of India to rescue it from mounting losses. What seemed like a straightforward administrative action turned into years of organizational turbulence. Employees from New Bank struggled to adjust, cultural differences created deep resentment, and litigation followed. For nearly three years, no internal promotions occurred at all.

That painful psu banks merger became a cautionary tale largely ignored in subsequent consolidations. When SBI absorbed its associate banks between 2008 and 2017, similar integration challenges emerged. Even today—more than a decade after some of those mergers—employees from erstwhile associate banks still feel undervalued within the larger structure. One senior banker put it bluntly: “A legal merger is not the same as an emotional merger.”

The 2019-20 consolidation drive, while impressive on paper, exposed fresh friction points. In one North Indian psu banks merger, the smaller bank had promoted an unusually high number of officers just before the merger, creating a cadre of relatively young executives holding senior designations. After integration, this disparity caused major heartburn within the parent bank, where officers saw their career prospects blocked by an influx of “younger seniors.” Promotion bottlenecks, posting disputes, and cultural clashes became routine complaints.

Which Banks Face the Merger Axe This Time?

According to government sources cited in recent Moneycontrol reports, four smaller public sector banks are prime psu banks merger candidates:

Indian Overseas Bank (IOB) with assets around ₹2.5 lakh crore could merge with State Bank of India, creating an even more dominant market leader.

Central Bank of India (₹3.8 lakh crore in assets) might fold into Punjab National Bank, strengthening PNB’s position as the second-largest PSB.

Bank of India (₹8 lakh crore) could combine with Bank of Baroda, creating a formidable third mega entity.

Bank of Maharashtra (₹2 lakh crore) might merge with Canara Bank, consolidating southern regional presence.

These potential psu banks merger combinations would reduce India’s public sector banking landscape to just six or seven major players: SBI, PNB, BoB, Canara Bank, Union Bank of India, and Indian Bank. The timeline remains uncertain, but internal discussions are expected to continue through FY27, with formal proposals possibly emerging within that fiscal year.

PSU Banks Merger: Government Plans Second Major Consolidation Round

The Real Challenges Nobody Prepared For

Every psu banks merger involves more than combining balance sheets—it’s a collision of cultures, histories, and employee aspirations. Several common problems have plagued past consolidations:

Promotion Policy Chaos: Different banks follow different grooming timelines. Smaller banks often promote officers faster, sometimes to higher grades, than larger institutions. When these disparate HR structures collide during a psu banks merger, resentment and demotivation follow inevitably.

Cultural Mismatches: Regional banks developed distinct work cultures over decades. A North Indian bank’s operational style differs dramatically from a South Indian institution. Forcing them together without cultural sensitivity creates friction that undermines productivity.

Technology Headaches: IT system integration represents one of the most underestimated challenges in any psu banks merger. Migrating customer data, reconciling different core banking platforms, and training staff on new systems takes years—not months.

Legacy Loyalties: Employees who spent entire careers building one institution don’t easily embrace a new identity. That emotional attachment gets dismissed as “sentimentality” by merger architects, but it shapes day-to-day workplace dynamics profoundly.

What Government Must Get Right This Time

If another round of psu banks merger moves forward, HR preparedness must come first—not as an afterthought. Banking expert Bikash Narayan Mishra, writing in India Today, suggests several critical steps:

Unified HR Vision: Before any public announcement, all stakeholders need agreement on clear roadmaps for postings, promotions, and performance appraisal systems.

Transparent Communication: Regular dialogues, detailed FAQs, and open forums should address employee concerns upfront. Silence breeds speculation and rumors that poison workplace morale.

Skill Alignment Programs: Focused training can bridge technological and cultural gaps between merging institutions. This means substantial investment in change management, not just technical training.

Mentorship and Integration Teams: Senior leaders from both sides working jointly can build trust and institutional camaraderie that top-down directives never achieve.

Recognition of Legacy Contributions: Employees from smaller banks shouldn’t feel merely absorbed—they should feel valued as co-creators of the new identity.

The Bigger Picture: Does Scale Always Win?

While the proposed psu banks merger focuses on creating globally competitive giants, success ultimately depends on people, not just capital adequacy ratios. A well-integrated, inspired workforce can transform even a modest-sized bank into a performance powerhouse. Conversely, a demoralized workforce can sink the mightiest institution, regardless of its balance sheet size.

Finance Minister Nirmala Sitharaman hasn’t officially commented on specific psu banks merger plans, but the broader government vision remains clear: fewer, stronger banks capable of driving India’s economic ambitions. Whether that vision translates into reality depends largely on how seriously authorities take the human integration challenge this time around.

For now, employees at potential psu banks merger candidates watch nervously, wondering whether their careers face another round of uncertainty. Bank unions are already raising concerns about promotion bottlenecks, forced transfers, and cultural displacement. The government’s response to these legitimate concerns will determine whether this consolidation drives genuine strength or simply creates larger, more dysfunctional institutions.

What Happens Next in the PSU Banks Merger Process

Any formal psu banks merger will require multiple approval stages:

Financial and Operational Assessments: Detailed due diligence on asset quality, liability structures, and operational compatibility.

Inter-Ministerial Consultations: Finance Ministry coordination with other government departments.

Bank Board Approvals: Individual bank boards must vote to approve merger proposals.

Cabinet and PMO Sign-off: Final political authorization from the highest levels.

RBI Fit-and-Proper Review: The central bank must certify that merged entities meet regulatory standards.

This multi-stage process typically takes 18-24 months from initial proposal to final implementation, assuming no major roadblocks emerge.

For comprehensive coverage of India’s banking sector reforms and the proposed psu banks merger, see these authoritative sources:

The Bottom Line: Can India Learn From Past PSU Banks Merger Mistakes?

The proposed psu banks merger represents either a bold step toward global competitiveness or a repeat of past integration failures—the outcome depends entirely on execution quality. Banking consolidation makes undeniable strategic sense in today’s competitive landscape. But without genuine commitment to human integration, transparent communication, and cultural sensitivity, this psu banks merger risks creating larger institutions plagued by the same internal dysfunction that undermined previous consolidations.

Policymakers should remember that mergers don’t just combine assets—they combine people, dreams, and decades of institutional identity. Getting that human equation right matters far more than any balance sheet arithmetic. Whether government officials have truly learned these lessons from past psu banks merger experiences remains the billion-dollar question as India’s banking sector awaits its next major transformation.