Are You Risking Your Family Business?

If your shop or family business runs as a partnership, registration may feel like extra paperwork you can delay. In India, partnership firm registration is not mandatory, but an unregistered firm loses key rights financial risk of not being able to recover dues or resolve disputes and it’s a loss This guide explains the real risks of staying unregistered, and a simple step-by-step process to register your firm with StartupMandi. By the end, you will know exactly how to protect your business, your relationships, and your profits.

Quick Summary

- Partnership firm registration in India is optional but almost mandatory in practice if you want full legal protection and growth.

- Unregistered firms can’t file cases to enforce contracts against customers or even between partners, which increases recovery and dispute risks.

- Registered firms enjoy better credibility, easier loans, smoother tax compliance, and stronger protection during disagreements.

- Small traders and family businesses should register early to avoid payment defaults, partner disputes.

What Is a Partnership Firm in India?

A partnership firm is a business where two or more persons agree to share profits of a business carried on by all or any of them acting for all, under the Indian Partnership Act, 1932. This agreement is usually recorded in a partnership deed, which defines partners’ rights, duties, and capital contribution.

How does partnership firm registration work?

Partnership firm registration means entering your firm’s details in the Register of Firms maintained by the state Registrar under Chapter VII of the Indian Partnership Act, 1932. After registration, the firm’s name and partners are officially recorded, and you get legal recognition that unlocks important rights under Section 69.

“For small and traditional businesses in India, a registered partnership is often the most practical step to gain legal identity without the complexity of a company.”

— Business compliance expert analysis

Is Partnership Firm Registration Mandatory in India?

No, registration of a partnership firm is not compulsory under the Indian Partnership Act, 1932. The law allows both registered and unregistered firms to exist, and you can legally operate your business even without registering the partnership.

However, an unregistered partnership firm faces serious legal restrictions under Section 69 of the Act, especially regarding filing suits in court to enforce contractual rights. In simple words, the law will still tax you, but it may not fully protect you if you stay unregistered.

What does Section 69 say about unregistered firms?

Section 69 of the Indian Partnership Act clearly states that:

- A partner of an unregistered firm cannot sue the firm or other partners to enforce rights arising from the contract.

- An unregistered firm cannot sue any third party to enforce a right arising from a contract (for example, unpaid invoices).

- The firm also cannot claim set-off (adjusting receivables against payables) in court beyond a very small amount.

That means if a customer refuses to pay a large bill, your unregistered firm may not be able to enforce that contract in court, even if your documents are clear.

What are the Risks And problems can an unregistered partnership firm face?

Unregistered partnership firms in India can face a mix of legal, financial, and practical risks that directly affect small traders and family businesses.

Here are the key risks explained:

- No right to sue customers for unpaid dues

An unregistered firm can’t file a suit in court to enforce contractual rights against a third party, including customers and suppliers. - Partners cannot sue each other for contract breaches

Partners of an unregistered firm cannot take legal action against each other to enforce rights under the partnership agreement, making disputes messy and emotional. This is especially risky in family businesses where disagreements can affect relationships for years. - Limited credibility with banks and vendors

Many lenders and large vendors prefer dealing with registered firms because they are more traceable and legally structured. An unregistered firm often struggles to get working capital loans, trade credit, or better payment terms. - Higher tax complications and scrutiny

While unregistered firms are still taxable, they may lose certain tax advantages and face more scrutiny from authorities because their existence is not properly documented with the Registrar. This can lead to longer assessments and possible penalties. - Difficulty entering tenders and big contracts

Government departments and large companies often insist on registration certificates or stronger structures like LLPs or companies. As an unregistered firm, you may be blocked from these opportunities even if you can deliver the work.

Comparison: Registered vs Unregistered Partnership Firms

“Registration of a partnership firm is not mandatory, but non-registration limits legal rights so severely that it is rarely advisable in practice.”

— Interpretation of Rest The Case’s legal guidance.

What Are the Benefits of Registering a Partnership Firm?

Why should small traders register their partnership firm?

For small traders and family-run businesses, registering the partnership firm converts an informal setup into a legally recognised business with more control and stability.

Key benefits include:

- Strong legal protection and enforceable rights

A registered firm can sue customers or partners to enforce contractual rights, recover money, and resolve disputes through courts if needed. This protection alone can save lakhs of rupees over the life of a business. - Better credibility and trust in the market

Registration signals seriousness and stability to landlords, suppliers, and bigger clients. It helps when negotiating credit terms, securing better shop premises, or onboarding corporate customers. - Smoother access to loans and finance

Banks and NBFCs are more comfortable lending to registered partnerships, especially when they see a clear deed and registration certificate. - Simplified tax filing and long-term compliance

Registration creates clarity about ownership and profit sharing, which simplifies tax returns and reduces future disputes about income allocation. It also supports smoother audits and less questioning from authorities. - Easier future conversion to LLP or company

If your business grows, you may convert into an LLP or private limited company for limited liability and funding. A registered partnership firm makes this conversion faster and more structured.

A survey of small businesses by compliance platforms in India has shown that firms with proper registrations and documentation are significantly more likely to secure institutional finance and formal contracts than purely informal setups. For a small trader, this can directly impact turnover and long-term survival.

Roadmap To Register a Partnership Firm in India (Actionable Guide)

How long does partnership firm registration take?

In most states, partnership firm registration can be completed within 7–21 working days, depending on document readiness and Registrar processing time. Delays usually happen due to incomplete documents or inconsistencies in deed details, which professional help can easily prevent.

What are the typical costs to register a partnership firm in India?

The total cost of partnership firm registration in India usually includes:

- Government fee for registration, which varies by state.

- Stamp duty on the partnership deed, which depends on your state and capital contribution.

- Professional fees (if you hire a consultant, CA, or platform like StartupMandi to manage the process). Total estimated cost roughly 120 USD( Which is nearly 11,000 rupees.)

Steps Include In This Registration Process

Below is a practical, extractable step-wise process for partnership firm registration in most Indian states.

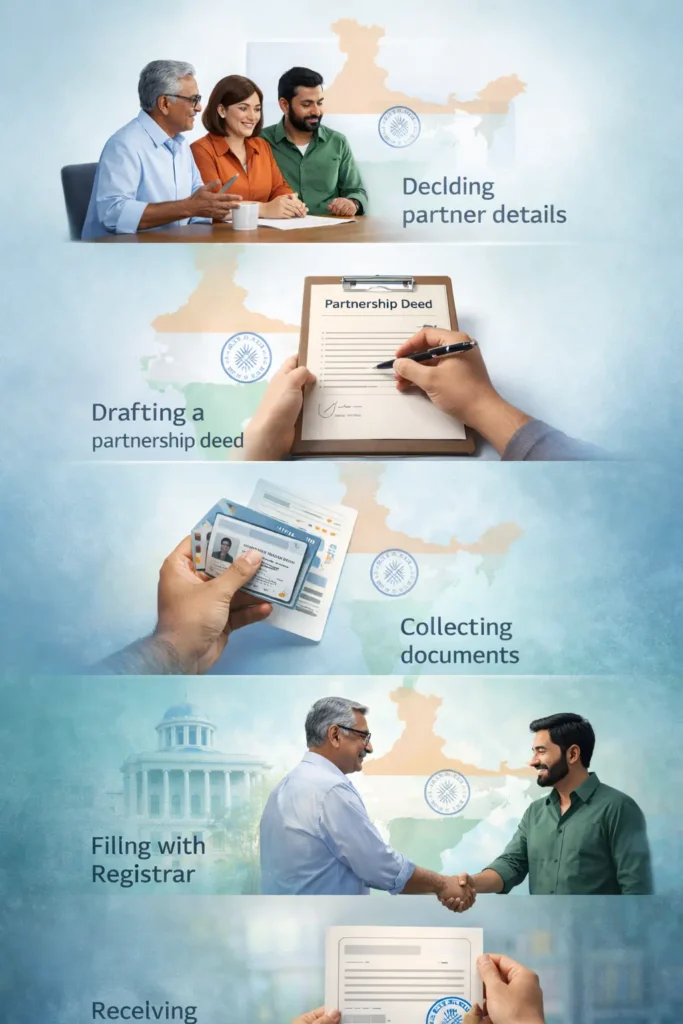

1. Decide key business details

Finalise the firm name, nature of business, principal place of business, capital contribution, and profit-sharing ratio among partners. Check that your selected name does not violate any trademark or restricted word rules.

2. Draft the partnership deed

Prepare a detailed partnership deed on appropriate stamp paper as per your state’s stamp law, including rights, duties, and exit terms. This can be done with help from a CA, CS, or legal expert for accuracy.

3. Get deed notarised or registered

Although not always compulsory, getting the deed notarised or registered with the Sub-Registrar adds evidentiary value during disputes. Many banks insist on a properly executed deed before opening a firm’s current account.

4. Collect KYC documents of partners and office

Gather PAN, Aadhaar, photos of partners, address proof of business place, electricity bill, and NOC from the owner if the premises are rented. Some states may ask for additional declarations or affidavits.

5. File application with Registrar of Firms

Submit Form I (or relevant state form) along with the partnership deed, KYC documents, and prescribed fees to the state Registrar of Firms. This can often be done through an authorised professional or online where available.

6. Receive Certificate of Registration

After verification, the Registrar records your firm in the Register of Firms and issues a Certificate of Registration or acknowledgment. From this point, your firm enjoys rights that unregistered firms do not get under Section 69.

7.Open current account and update stakeholders After registration, open a current account in the firm’s name and update vendors, customers, and tax authorities with new details.

documents needed to register a partnership firm

Most states in India require a similar document set for partnership firm registration.

You typically need:

- Partnership deed (signed by all partners, on stamp paper as per state law).

- PAN cards of all partners and of the firm (if available at that stage).

- Address proof of partners (Aadhaar, voter ID, passport, etc.).

- Business address proof (electricity bill, rent agreement, property tax receipt, or sale deed).

- Passport-size photographs of all partners.

- NOC from property owner if the office/shop is on rented premises.

Some states may also ask for an affidavit stating that the details provided are true and that the firm’s name is unique within the state Register.

Tools You Need:

Partnership deed drafting software, Document scanner app, Government registration portal, Professional consultancy platform (e.g., StartupMandi can help you complete this end-to-end registration through a simple, guided process, so you avoid rejections and missing documents.)

Key Takeaways

- Partnership firm registration is voluntary in law but essential in practice because unregistered firms lose key legal rights, especially under Section 69.

- Unregistered firms face real risks: they cannot sue for unpaid bills, partners cannot enforce rights against each other, and credibility suffers with banks and bigger clients.

- Registration offers legal protection, stronger reputation, easier loans, and smoother tax compliance, which directly supports business growth.

- The process is straightforward and affordable when handled with expert help, especially for small traders and family businesses that cannot afford long disputes.

For your shop or family-run business, the cost of registration is small compare to the potential loss from one large unpaid invoice or major partner dispute.

Next Steps

- Review your current partnership setup and check whether your firm is actually registered with the Registrar of Firms in your state.

- If you are unregistered, plan to draft or upgrade your partnership deed so it reflects current partners, capital, and roles.

- Collect KYC and business address proofs in one place to speed up the registration process.

- Reach out to StartupMandi to get a guide partnership firm registration service tailored for small traders and family businesses.

- After registration, align other compliances like GST, Shop and Establishment, and bank accounts for a fully compliant, growth-ready business structure.

A soft but important reminder: registering your partnership is not a luxury; it is a safety net that protects your livelihood and relationships.

“In small businesses, a single legal mistake can wipe out years of hard work. Registration is the cheapest insurance you will ever buy.”

— Adapted from guidance by Indian small business compliance experts

Conclusion

Partnership firm registration in India may be legally optional, but for small traders, wholesalers, and family businesses, it is the practical line between an informal setup and a protected, growth-ready organisation. By registering your firm, you gain the right to enforce contracts, build trust with banks and suppliers, and minimise the damage of future disputes.

StartupMandi can help you move from risk to security with a simple, guided partnership registration service designed for small and traditional businesses. Explore our guides on GST registration and MSME registration to complete your compliance stack and unlock more benefits for your growing business.

FAQs

Is partnership firm registration compulsory in India?

No, but you may loose your right to sue customers and partners, so registration is strongly recommended for small traders.

Can an unregistered partnership firm sue for recovery of money?

NO, It cannot file a suit in court to enforce contractual rights against third parties, including recovery of unpaid invoices

Can an unregistered partnership firm be taxed by the Income Tax Department?

Yes, they are still subject to income tax.

Is partnership deed registration the same as partnership firm registration?

No, registering a deed mainly improves evidence value, while firm registration provides legal rights under Section 69.

How many partners are require to start a partnership firm in India?

At least two persons can form a partnership under the Indian Partnership Act, 1932.

Can a partnership firm be convert into an LLP or private limited company later?

Yes, many businesses start as partnerships and later convert to LLPs or companies for limited liability and funding advantages.

Is GST registration require along with partnership firm registration?

It depends on your turnover and type of business; many traders need both to operate smoothly and claim input tax credit.

How can StartupMandi help with partnership firm registration?

They can guide you on deed drafting, documentation, filing with the Registrar, helping you avoid , delays, and compliance gaps while you focus on running your business.

A Few suggested Links For Further Research And Facts Check

- Is registration of partnership firm compulsory in India?

- “Section 69 of the Indian Partnership Act, 1932 – Effect of non-registration “

- “Consequences of not registering a partnership firm in India”

- “Top benefits of registration of partnership firm in India”

- “Registration of partnership firm in India and effect of non-registration”

Thanks for highlighting the importance of partnership firm registration—especially the risks of staying unregistered, like being unable to sue in court or recover dues. It’s a practical reminder that while registration isn’t mandatory, it’s a crucial step for long-term business security and clarity. The step-by-step process you shared makes it easier to take that next step if needed.

Thank you for your comment. To use your site link & generate backlink on our platform, 1st go through a paid plan on this page: https://startupmandi.in/services/digital-services/premium-brand-promotion-on-startupmandi/

Thanks for highlighting the importance of partnership firm registration—especially the risks of staying unregistered, like being unable to sue in court or recover dues. It’s a practical reminder that while registration isn’t mandatory, it’s a crucial step for long-term business security and peace of mind. The step-by-step process you outlined makes it easier to take that next step.

Thank you for your comment. To use your site link & generate backlink on our platform, 1st go through a paid plan on this page: https://startupmandi.in/services/digital-services/premium-brand-promotion-on-startupmandi/

Thanks for highlighting the importance of partnership firm registration, especially since the recent update about new registrations being paused. It’s a timely reminder that while registration isn’t mandatory, skipping it can leave your business vulnerable to legal disputes and financial risks. The step-by-step process you’ve outlined will definitely help entrepreneurs make informed decisions about their business structure.

Thanks for highlighting the importance of partnership firm registration—especially the risks of staying unregistered, like being unable to sue in court or recover dues. It’s a crucial step for long-term business protection, even though it might feel like extra work. The process you outlined is clear and helpful for those considering this move.

Thank you for your comment. To use your site link & generate backlink on our platform, 1st go through a paid plan: https://startupmandi.in/services/digital-services/premium-brand-promotion-on-startupmandi/