Business Loan India 2026: Easy Step-by-Step Guide

Access to capital remains crucial for business growth and expansion in India. Moreover, the business loan landscape in 2026 has become more streamlined and accessible than ever before. Whether you’re a startup founder, MSME owner, or established entrepreneur, getting a business loan is no longer a daunting task. Furthermore, with digital platforms, government schemes, and competitive lending options, entrepreneurs can secure funding quickly and efficiently. This comprehensive guide walks you through the entire process of obtaining a business loan easily in India, covering eligibility criteria, documentation, application steps, and expert tips to boost approval chances.

Business loan application process in India 2026

Understanding Business Loan India 2026

Business Loan India 2026 serve as financial lifelines that help entrepreneurs manage working capital, purchase equipment, expand operations, or meet urgent business needs. In India, business loans are offered by banks, Non-Banking Financial Companies (NBFCs), and government-backed schemes. Consequently, the market has evolved significantly, offering unsecured loans with minimal documentation and faster approvals within 48 hours.

Types of Business Loans Available

Various loan types cater to different business needs. Therefore, understanding these options helps you choose the right financing solution.

Working Capital Loans provide funds for day-to-day operational expenses like salaries, rent, and inventory purchases. Additionally, Term Loans offer fixed-duration financing for major investments such as expansion or asset acquisition, available in both short-term and long-term variants. Meanwhile, Equipment Finance helps businesses upgrade machinery and improve productivity. Furthermore, Invoice Financing enables companies to access instant cash against unpaid customer invoices. Similarly, Overdraft Facilities allow withdrawals beyond current account balances up to approved limits.

Government-backed schemes also play a vital role. Specifically, Mudra Loans under PMMY support micro-enterprises with collateral-free loans up to ₹20 lakh. Additionally, CGTMSE Loans provide collateral-free financing up to ₹2 crore with government guarantees. Moreover, SIDBI Loans offer specialized financing from ₹3 crore to ₹50 crore for MSMEs. Check what ClearTax is saying about this.

Key Eligibility Requirements for Business Loan India 2026

Meeting eligibility criteria significantly increases approval chances. Therefore, lenders evaluate multiple factors before sanctioning loans. Check DMI-Finance’s article.

Basic Eligibility Criteria

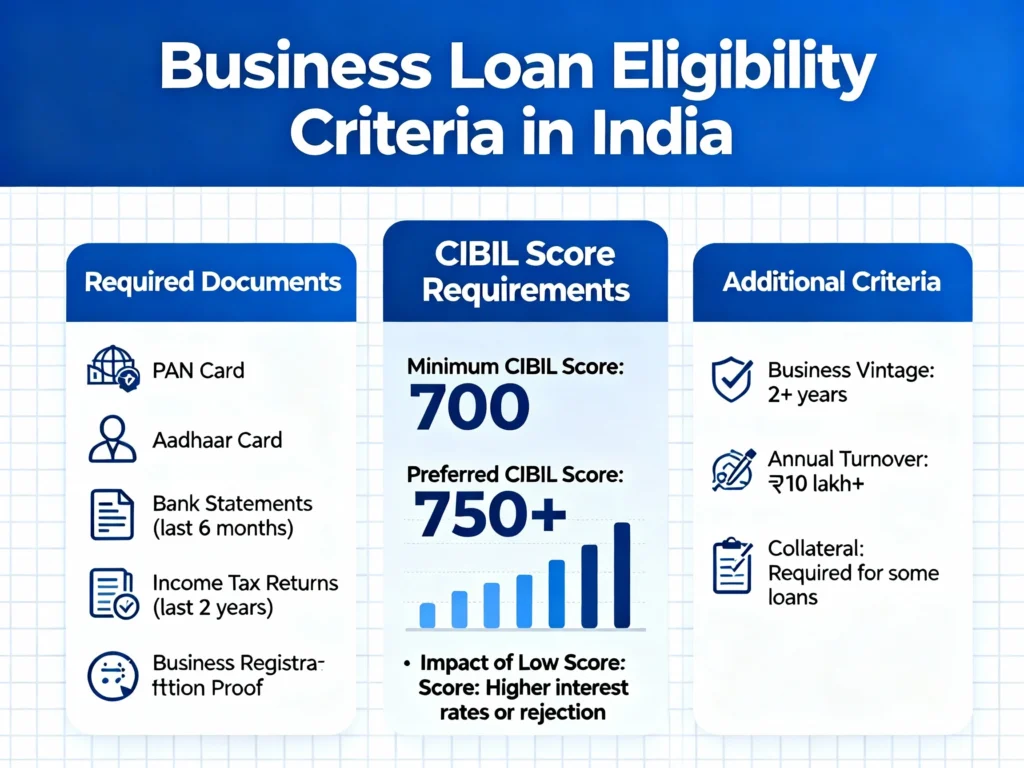

First and foremost, applicants must be Indian nationals between 21 and 80 years of age. Additionally, the business should have operated for at least 2-3 years minimum. Furthermore, a CIBIL score of 685 or higher is typically required, though some lenders like DMI Finance accept scores of 700+. Similarly, annual turnover should range from ₹3 lakh to ₹10 lakh minimum depending on the lender. Moreover, applicants must be self-employed individuals, business owners, or proprietors. Check Business Loans from Bajaj Finance.

Business Entity Types

Different business structures qualify for loans. Consequently, sole proprietorships, partnership firms, private limited companies, public limited companies, and LLPs are all eligible. Additionally, self-employed professionals like doctors, architects, and consultants can apply. Furthermore, MSMEs registered under MSME norms qualify for special schemes. Check Business Loans from Sriram Finance.

Business loan eligibility requirements and documentation

Required Documents for Business Loan Application

Proper documentation ensures faster approval and prevents rejection. Therefore, having all documents ready beforehand streamlines the process. Learn more from Finvest.

Essential Documentation

Identity and Address Proof includes Aadhaar card, passport, voter ID, or driving license. Additionally, Business Registration Documents comprise business licenses, GST/VAT certificates, and trade licenses. Furthermore, Financial Statements require balance sheets and profit & loss statements for the last 2-3 years. Similarly, Bank Statements from the last 6-12 months demonstrate cash flow patterns. Moreover, Income Tax Returns for both business and personal accounts from the previous 2-3 years are mandatory. Additionally, PAN Cards for both personal and business entities are required. Finally, GST Registration certificates are preferred though not always mandatory.

Step-by-Step Process to Get Business Loan Easily

Following a structured approach simplifies the application journey. Therefore, breaking down the process into clear steps helps ensure success.

Successful business loan approval in India

Step 1: Determine Your Funding Needs

Initially, calculate the exact loan amount required for your business purpose. Additionally, create realistic financial projections including operational costs and expansion plans. Furthermore, avoid overborrowing as it increases repayment burden.

Step 2: Check Your Eligibility

Subsequently, verify that you meet the minimum age, business vintage, and credit score requirements. Moreover, review your CIBIL score and address any discrepancies before applying. Additionally, ensure your business turnover meets lender thresholds.

Step 3: Compare Lenders and Loan Options

Next, research various banks, NBFCs, and online lenders to find competitive rates. Furthermore, compare interest rates, processing fees, and prepayment charges across multiple lenders. Additionally, evaluate loan terms, tenure options, and hidden costs. Meanwhile, consider government schemes like Mudra loans for better terms.

Step 4: Gather Required Documents

Then, compile all necessary documents including KYC, business proof, financial statements, and bank statements. Additionally, prepare a comprehensive business plan outlining goals, strategies, and financial projections. Furthermore, ensure all documents are accurate and up-to-date to avoid delays.

Step 5: Submit Your Application

After preparation, visit the lender’s website or download their mobile app. Subsequently, register using your mobile number and verify with OTP. Then, fill in the application form with personal and business details. Next, upload all required documents through the digital platform. Finally, submit your application for processing.

Step 6: Application Review and Verification

Following submission, lenders verify documents and assess creditworthiness. Additionally, they conduct background checks and may request clarifications. Furthermore, a representative may contact you for additional information or verification. Therefore, respond promptly to queries to expedite approval.

Step 7: Loan Approval and Disbursal

Upon approval, carefully review the loan agreement terms. Subsequently, sign the agreement digitally or physically as per lender requirements. Finally, the loan amount is credited to your bank account within 24-72 hours.

Interest Rates and Charges for Business Loans

Understanding costs helps in financial planning and choosing the right lender. Therefore, comparing rates and fees is crucial.

Business loan interest rates in India typically range from 8% to 30% per annum depending on various factors. Additionally, processing fees can go up to 4.72% of the loan amount. Furthermore, bounce charges of approximately ₹1,500 per instance apply for failed EMI payments. Moreover, prepayment charges up to 4.72% may be levied for early loan closure.

Several factors influence your interest rate. Specifically, credit scores above 750 qualify for lower rates. Additionally, longer business vintage reduces perceived risk. Furthermore, higher loan amounts may attract better rates. Moreover, collateral-backed loans typically have lower interest rates than unsecured loans.

Government Schemes for Business Loans in 2026

Government initiatives provide accessible and affordable financing options. Therefore, exploring these schemes can offer significant advantages.

The Pradhan Mantri Mudra Yojana (PMMY) offers collateral-free loans categorized into four segments. Specifically, Shishu provides up to ₹50,000 for budding entrepreneurs. Meanwhile, Kishore offers ₹50,001 to ₹5 lakh for growing businesses. Additionally, Tarun provides ₹5 lakh to ₹10 lakh for established enterprises. Furthermore, Tarun Plus extends ₹10 lakh to ₹20 lakh for successful previous borrowers.

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) offers collateral-free loans up to ₹2 crore with 75-90% government guarantee coverage. Moreover, the MSME Loan in 59 Minutes scheme provides fast-tracked online processing for loans up to ₹5 crore. Additionally, SIDBI Loans support MSMEs with specialized financing from ₹3 crore to ₹50 crore for machinery, expansion, and working capital needs.

Tips to Improve Your Business Loan Approval Chances

Implementing strategic measures significantly enhances approval probability. Therefore, following these expert recommendations is essential.

Maintain a Strong Credit Score

Primarily, pay all EMIs and credit card bills on time consistently. Additionally, keep credit utilization below 30% of available limits. Furthermore, avoid applying for multiple loans simultaneously as it signals financial stress. Moreover, regularly check your credit report for errors and dispute inaccuracies promptly. Additionally, maintain a healthy mix of secured and unsecured credit.

Strengthen Your Financial Profile

Subsequently, file GST and income tax returns regularly and on time. Additionally, separate business and personal finances for clear financial tracking. Furthermore, maintain consistent revenue streams and demonstrate profitability. Moreover, build a strong business credit history through timely vendor payments. Finally, prepare detailed financial projections showing repayment capacity.

Optimize Your Application

Furthermore, prepare a comprehensive business plan demonstrating clear goals and strategies. Additionally, provide complete and accurate documentation to avoid delays. Moreover, be transparent with lenders about your financial situation. Finally, choose the appropriate loan type matching your specific business needs.

Common Mistakes to Avoid When Applying

Avoiding pitfalls prevents rejection and ensures smooth processing. Therefore, awareness of common errors is critical.

Firstly, lacking a clear business plan weakens your application significantly. Additionally, neglecting to check your credit score beforehand often leads to rejection. Furthermore, submitting incomplete documentation causes unnecessary delays. Moreover, borrowing more or less than required creates financial strain. Similarly, ignoring hidden charges and fees increases overall costs. Additionally, focusing solely on interest rates without considering total loan cost is misleading. Furthermore, not comparing multiple lenders limits your options. Moreover, ignoring repayment capacity leads to default risks. Finally, choosing the wrong loan type for your business needs wastes resources.

Strategies for Efficient Loan Repayment

Managing repayment effectively maintains financial health and creditworthiness. Therefore, implementing smart strategies is essential.

Initially, use business loan EMI calculators to plan repayments accurately. Additionally, set up automated payments to avoid missed deadlines. Furthermore, pay more than the minimum EMI whenever possible to reduce tenure and interest. Moreover, consider refinancing if better rates become available. Additionally, create a structured repayment plan aligned with cash flow cycles. Furthermore, reduce unnecessary expenses to free up funds for EMIs. Finally, maintain emergency reserves to handle unexpected business challenges.

Conclusion

Securing a business loan in India in 2026 has become significantly easier with digital platforms, streamlined processes, and competitive lending options. By understanding eligibility criteria, preparing proper documentation, maintaining a strong credit profile, and choosing the right lender, entrepreneurs can access funding quickly and efficiently. Moreover, government schemes like Mudra loans and CGTMSE provide excellent alternatives for collateral-free financing. Therefore, following the step-by-step process outlined in this guide ensures a smooth loan application journey.

StartupMandi is your trusted partner in navigating the complex business landscape in India. We provide comprehensive resources, expert guidance, and end-to-end support for entrepreneurs seeking business loans and financial solutions. Our platform connects you with verified lenders, helps you understand eligibility requirements, and offers personalized assistance throughout the application process. Additionally, we offer services including business registration, compliance management, financial planning, and growth strategy consultation. Visit StartupMandi today to explore our services and take your business to the next level.

For more valuable insights on business growth and financing, check out our related articles:

- Top Government Schemes for Startups in India

- How to Improve Your Business Credit Score

- Complete Guide to MSME Registration

Frequently Asked Questions (FAQs)

Q1. What is the minimum CIBIL score required for a business loan in India?

Most lenders require a minimum CIBIL score of 685 to 750 for business loan approval. However, some NBFCs like DMI Finance accept scores of 700 and above. A higher credit score significantly improves your chances of approval and helps secure lower interest rates.

Q2. How long does it take to get a business loan approved in India?

With digital platforms and streamlined processes, business loan approvals now take between 24 to 72 hours after document verification. Some lenders offer instant approvals through their mobile apps. The MSME Loan in 59 Minutes scheme provides even faster processing for eligible applicants.

Q3. Can I get a business loan without collateral in 2026?

Yes, numerous lenders offer unsecured business loans without requiring collateral. Government schemes like Mudra loans and CGTMSE provide collateral-free financing up to ₹2 crore. NBFCs and banks also offer unsecured loans based on creditworthiness, business performance, and repayment history.

Q4. What documents are mandatory for business loan applications?

Essential documents include KYC documents (Aadhaar, PAN), business registration proof, financial statements for 2-3 years, bank statements for 6-12 months, income tax returns, and GST registration. Having these documents ready beforehand ensures faster approval.

Q5. How can I improve my chances of business loan approval?

Maintain a strong CIBIL score above 750, file tax returns regularly, keep credit utilization below 30%, prepare a comprehensive business plan, ensure complete documentation, demonstrate consistent revenue streams, and choose the right loan type matching your business needs. Additionally, avoid applying for multiple loans simultaneously.